The Vampire Squid Occupies Trump's White House

Back on February 19th, during a primary-season speech in Myrtle Beach, South Carolina, Donald Trump directed a two-pronged rhetorical offensive against opponents in both parties. He started with Ted Cruz.

Cruz's campaign, Trump pointed out, had taken loans from the infamous investment bank Goldman Sachs. And he'd failed to properly disclose one of these loans.

"I know the guys at Goldman Sachs. They have total, total control over ," Trump said. "Just like they have total control over Hillary Clinton."

Trump demonized the bank enough that it almost seemed like genuine animosity existed between candidate and squid. When Goldman announced in September that it was banning employees from donating to Trump's campaign, it seemed official.

In October, Trump was even more specific in pointing the finger at Goldman. Referencing speeches Clinton gave to Goldman, Trump said that "Hillary Clinton meets in secret with international banks to plot the destruction of U.S. sovereignty in order to enrich these global financial powers, her special interest friends and her donors."

Trump's tales sounded like classic Rothschild/Bilderberg conspiracy lore. They would have been absurd, were it not for the fact that so much of the innuendo around Goldman Sachs often turns out to be true.

The bank has an extraordinary history of placing its executives in high-ranking governmental and quasi-governmental positions, from treasury secretaries to senators to the heads of the World and European Central Banks. Goldman has been implicated in the trafficking of toxic mortgages, a sprawling state corruption case in Malaysia, the manipulation of world commodity prices and a heinous episode involving Greece in which the bank helped to mask the country's ballooning debt while simultaneously working with JPMorgan Chase to create an index for betting against Greece's economy.

Nonetheless, Trump's insinuations about a Goldman-Hillary secret conspiracy were so pointed that CEO Lloyd Blankfein was forced to respond.

"If there's some secret international cabal, I've been left out of the party again," he quipped.

In his final pitch to voters in the days before the election, Trump used the image of Blankfein in a TV ad to argue that insiders had ruined the lives of ordinary Americans to enrich themselves. Here is the narration you heard when Blankfein's face came on screen:

"It's a global power structure that is responsible for the economic decisions that have robbed our working class, stripped our country of its wealth and put that money into the pockets of a handful of large corporations and political entities."

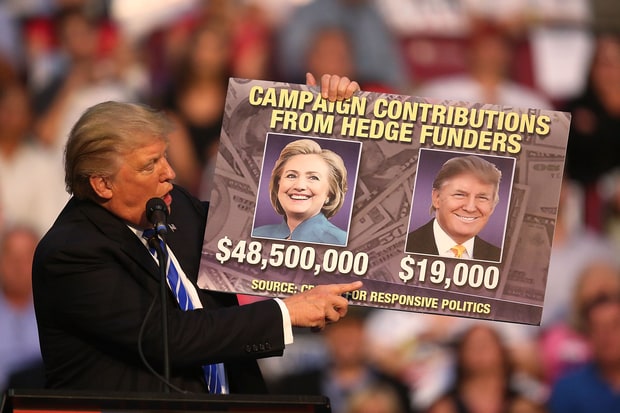

Trump at an August campaign rally in Fort Lauderdale, Florida. Joe Raedle/Getty

One surprise election result and a mountain of jubilant #draintheswamp hashtags later, Donald Trump has filled his White House with, you guessed it, Goldman veterans.

His chief strategist, the unabashed white-supremacist loon Steve Bannon, is a former Goldman banker, as is adviser Anthony Scaramucci. Steve Mnuchin marks the fourth Goldman-pedigreed treasury secretary in the last four presidencies, after Bob Rubin, Lawrence Summers and Hank Paulson.

But the real shocker is the recent appointment of Goldman Chief Operating Officer Gary Cohn to the post of director of the National Economic Council. Bannon and Mnuchin were former, past Goldmanites. Cohn, meanwhile, is undoubtedly at least the number-two figure at the world's most despised bank, if not the outright co-head with Blankfein. He has been at the center of many of its most infamous episodes, including the Greek affair.

So much for draining the swamp.

The new party line, emanating both from Washington and from Alt-Right yahoos on the Internet, is that people like Gary Cohn are no longer the swindling scum-lords Trump said they were a few months ago, but simply smart businessmen.

As Trump put it, "Gary Cohn is going to put his talents as a highly successful businessman to work for the American people."

This mantra is often used to explain Goldman's legend. Its advocates say they may be cold-blooded, but they're just dern good at what they do.

The bank has worked very hard to nurture exactly that image, particularly when there are darker explanations for the bank's success that they would rather leave unexplored. A great example involves Cohn, Trump's new "top economic adviser."

Way back in November of 2007, a tidal wave was beginning to devour Wall Street. The subprime mortgage market was collapsing, and the bulk of America's investment banks were foundering.

Indeed, within a year, three of the country's storied top five investment banks – Bear Stearns, Merrill Lynch and Lehman Brothers – would be wiped out by the crisis, thanks mainly to their overinvestment in subprime.

One bank stood out as an exception: Goldman Sachs.

The legend on the street was that Goldman was somehow not only going to survive the crash, but prosper and make big profits. How did Goldman do so well during a financial hurricane? The New York Times had an answer: its leaders were smart – and humble!

"Goldman's secret sauce, say executives, analysts and historians," the paper wrote, "is high-octane business acumen, tempered with paranoia and institutionally encouraged — though not always observed — humility."

Where did writers Jenny Anderson and Landon Thomas Jr. get the idea that Goldman's smarts saved them during the mortgage crisis? From Goldman, of course.

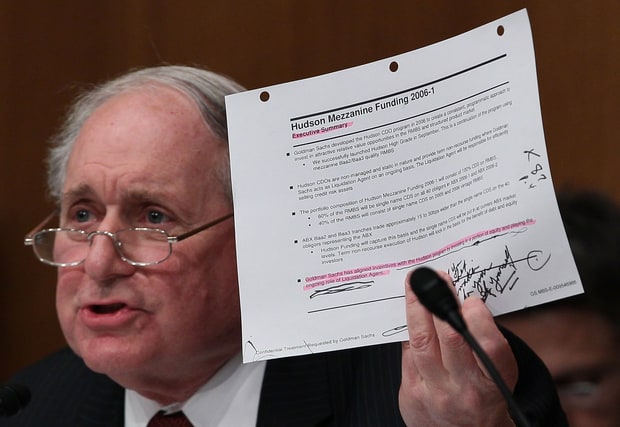

We know this because of an investigation conducted into the bank's a-little-too-miraculous performance that year by the Senate Permanent Subcommittee on Investigations.

Chaired by Michigan Sen. Carl Levin, the PSI scrupulously detailed the efforts by Goldman to get out from under the mortgage crash by dumping its disastrous mortgage investments on its own clients as it simultaneously bet against them.

This maneuver, colloquially described since as the "Big Short" episode, was perhaps the most lurid example of Wall Street iniquity during the crash years. And Trump's new economic adviser, Cohn, played a central role.

Michigan Senator Carl Levin. Mark Wilson/Getty

In the run-up to the "Big Short" story – in the years leading up to 2007 – Goldman had joined other banks in helping cause the financial crisis. They'd done so by creating masses of toxic mortgage instruments and selling them to unsuspecting investors, who were (often falsely) told the loans met underwriting standards. Goldman, like JPMorgan Chase, Bank of America and Citigroup, would later pay billions to settle claims by its infuriated customers, which included state and federal housing authorities.

At the tail end of 2006, Goldman execs saw that a) the subprime mortgage market was in serious trouble, and b) the bank itself was dangerously overinvested in it. So they made a frenzied, often deceptive effort to induce their clients to eat what should naturally have been their own losses.

On December 14th, 2006, mortgage chief Daniel Sparks proposed: "Distribute as much as possible on bonds created from new loan securitizations and clean previous positions."

Translation: Let's create new mortgage-backed products to dump on others, and use them to "clean" our toxic portfolio.

In one mortgage-based deal called Hudson 1 securities, Goldman helped sell its toxic holdings by saying the bank's interests were "aligned" with those of potential clients, because it would own a tiny, $6 million slice of the deal.

The bank left out the fact that it had a $2 billion bet against the same deal.

In the same deal, Goldman told clients that the mortgage products in Hudson had been "sourced from the Street," i.e., that this stuff did not come from Goldman's own inventory. When Senate investigators later pressed Goldman executives on this question, they hilariously claimed this wasn't a lie, because Goldman was part of "the Street."

"They were like, 'We are the Street,'" one investigator told me, laughing.

Through deals like this, Goldman within months went from having a $6 billion bet on mortgages to having a $10 billion bet against them – a "big short."

All of these moves were made with the assent of the Firmwide Risk Committee, which included Goldman CFO David Viniar, Blankfein and Cohn.

They would go on to fleece other clients. In the summer, an Australian hedge fund called Basis Capital was induced to buy $100 million of a mortgage-based Goldman deal called "Timberwolf." They told the Aussies to expect a return of "over 60 percent."

Meanwhile, in private, Goldman execs were saying things like, "Boy, that timberwof was one shitty deal."

The sales rep who got Basis to buy was so elated that the subject line of his email read "Utopia." He told other execs he'd found the ultimate sucker. "I found white elephant, flying pig and unicorn all at once," he crowed.

Basis Capital later claimed it lost $56 million in six weeks. It filed for bankruptcy within months of the Timberwolf deal.

Getting back to the Times story about how Goldman's smarts and humility saved them during the crash: One of the documents the Senate investigators discovered was an email from Goldman press flack Lucas van Praag to a group of senior Goldman executives that included Blankfein, Cohn and Viniar.

Van Praag wanted to warn the leadership that there was a Times piece coming that would examine why Goldman managed to prosper at a time when everyone else was being wiped out. Van Praag did not, of course, tell The Times that Goldman had survived by making sure that its clientele bought up what Blankfein called the "cats and dogs" of its toxic inventory.

What van Praag instead said was more Trumpian: that Goldman just had a winning culture.

"We spent a lot of time on culture as a differentiator," van Praag told his bosses, when describing his interactions with apparently gullible reporter Jenny Anderson. "She was receptive."

In response to van Praag's email, Blankfein wrote, "Of course we didn't dodge the mortgage mess. We lost money, then made more than we lost because of shorts."

This is the same Lloyd Blankfein who testified years later in the Senate: "We were not consistently or significantly net-short the market in residential mortgage-related products in 2007 and 2008."

He added, "We didn't have a massive short against the housing market, and we certainly did not bet against our clients."

When Sen. Levin heard Blankfein say he didn't have a "massive short" during 2007, he was furious. "Heck, yes, I was offended," he told Rolling Stone. "Goldman's CEO claimed the firm 'didn't have a massive short,' when the opposite was true."

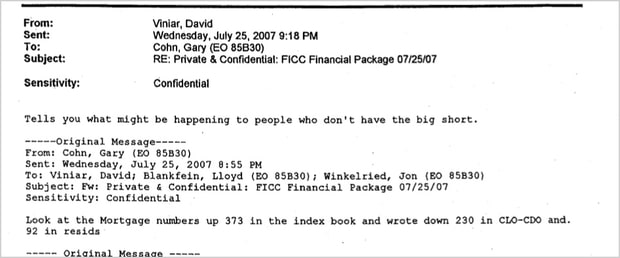

We know the "opposite was true" because of the extensive email record these arrogant yutzes left behind. One of the smoking guns involved Cohn. On July 25, 2007, Viniar sent Cohn an email pointing out the huge losses and writedowns that other banks were experiencing.

"Tells you what might be happening to people who don't have the big short," Viniar told Cohn.

In the heat of the meltdown, there was some gallows humor between Cohn and Blankfein. At one point the two men seemed to be trying to figure out where they were with their mortgage strategy, and what to do going forward. "We are marking both sides," Cohn says. "There is a net short."

"Bet all the dads at camp are talking about the same stuff," Blankfein joked.

Goldman's higher-ups ended up having a great year. While the whole financial world was collapsing due in large part to behaviors like that of his own bank, Blankfein made $68.5 million, a record for a Wall Street executive. Cohn made $67.5 million. The two were the McGwire and Sosa of the profiting-off-others'-misery era. The bank, meanwhile, would lay off 3,200 lower-level employees within a year.

Goldman probably should have gone out of business in 2007-2008. Two little-discussed acts of government welfare in September of 2008 helped save the company.

First, there was the infamous emergency granting of Commercial Bank Holding Company status to Goldman. Have you ever seen a Goldman branch or a Goldman ATM? Probably not, because it isn't a commercial bank. But on September 21st, 2008, the government gave it permission to call itself one.

This move, so desperately needed that it was executed on a Sunday night, allowed Goldman access to mountains of life-saving cash from the Federal Reserve.

The other key move was a decision by the SEC to ban short-selling of financial stocks. This nakedly anticapitalist maneuver allowed Goldman to fend off attacks by speculators who correctly sensed the company was in deep trouble.

Apart from the SEC order, major shareholders like pension funds in New York and California also agreed to stop lending shares of Goldman and Morgan Stanley to short-sellers, essentially protecting these two banks in particular from the forces of the market. Notably, they were the two top-five investment banks that survived 2008.

Blankfein was initially opposed – "I'm for markets," he reportedly said – but as things worsened, he agreed with Morgan Stanley chief John Mack that they needed their government Daddy to save them.

"You're right. We have to do something about this," he said. He later called the decision "tricky."

Yet even with the SEC ban on short-selling, Goldman's stock price continued to plunge, from $207.78 in February 2008 to $47.41 in November. Cohn claims not to have been worried. "It wasn't scary at all," he said.

Vanity Fair found a colleague who scoffed at Cohn's assessment. "Complete and utter nonsense," the person said. For all their brains and humility, these geniuses needed the government to halt the free market on their behalf to survive.

Goldman deserves its villainous reputation. The bank symbolizes all the worst aspects of the modern "financialized" economy. The crash era was the ultimate example.

Banks like Goldman mostly didn't create anything of value during this time. Mostly what they did was engineer new ways to create credit that led to millions of people buying homes they couldn't afford, creating the mother of all financial bubbles.

When it all went bust, as it necessarily had to, they scrambled by hook or crook to dump the damage on other people. Clients ate their losses and they ran weeping to the taxpayer for rescue – Goldman got $12.9 billion alone just from the AIG bailout, which of course was engineered by former Goldman chief Hank Paulson. In the middle of all of this, people like Blankfein and Cohn paid themselves record amounts of compensation. They are scum, and it's absolutely fitting that so many of them will end up serving the Trump administration.

Donald Trump made a lot of political hay out of the iniquity of people like Cohn during his campaign. But his recent appointments are absolute proof that his "populist" message was a crock all along – not that we couldn't have guessed anyway.