Did the Pandemic Finally Give Working Americans Power Over Their Employers? Not Really

Labor advocates have been feeling their oats lately, what with a surge of successful union organizing drives at Starbucks stores, the hint of union interest at Amazon warehouses, higher minimum wage standards in cities and states across the country, and a nudge up of average wages across the board.

These trends have inspired some to proclaim the advent of a new era of worker power.

“The labor market is experiencing a Great Upgrade,” the progressive Roosevelt Institute declared in February.

“We’re in a moment where, politically, workers are ascendant,” David Madland of the Center for American Progress, a liberal think tank, told the investment publication Barron’s in May. (The article’s headline read: “How Workers Gained an Edge — and Why They Won’t Lose It Soon.”)

Unfortunately, this sort of confidence can be a drug that invites dangerous overdoses. That’s the view of economist Teresa Ghilarducci of the New School.

Ghilarducci recently compiled a roster of economic indicators suggesting that workers haven’t gained as much leverage as a superficial examination might suggest. Even the advances thus far, such as they are, still leave miles to travel before the American working class recovers all the economic standing it has lost since the 1970s.

“A lot of the talk about labor having power is based on organizing efforts at Starbucks and Amazon,” Ghilarducci told me. Of 11 economic indicators she examined, she says, “most indicators show either declining labor power or give mixed signals.”

Ghilarducci is not aiming to be a killjoy just for the hell of it. The condition of the labor market is critically important because the Federal Reserve Board is convinced that the tight labor market is an important factor driving inflation higher. Consequently, its inflation-fighting approach involves kneecapping worker bargaining power.

Fed Chairman Jerome H. Powell has explicitly stated that unemployment must rise for inflation to come down. “The labor market has remained extremely tight,” Powell said at his Sept. 21 news conference after the Fed’s monthly decision to raise interest rates by three-quarters of a percentage point for the third time in a row.

As evidence for the tight labor market, Powell cited “the unemployment rate near a 50-year low, job vacancies near historical highs, and wage growth elevated ... with demand for workers substantially exceeding the supply of available workers.” He concluded, with evident regret, “So far, there’s only modest evidence that the labor market is cooling off.”

Yet if the labor market hasn’t been tight enough to provide workers with real gains in wages and living standards, the Fed’s approach threatens to take away the lackluster gains they have achieved in the last year.

So let’s examine what has really been happening on the labor front.

The most important indicator is wage growth. Although pay has been rising, wages have been outstripped by price inflation. In raw terms, average nonfarm hourly wages rose by 5.2% in the year that ended in August, according to the Bureau of Labor Statistics. In real terms, however — that is, accounting for inflation — they fell by 2.8% in that period.

The Fed’s approach is based on an economic concept known as the Phillips curve, which posits a concrete relationship between unemployment and inflation (as unemployment rises, inflation falls and vice versa).

As I reported previously, though, this is a mechanistic approach that harks back to pre-Depression policy, when working men and women were regarded as just another economic input and downturns were valued as necessary medicine to preserve the financial well-being of the bondholding class.

It was the era when the prescription for an economic downturn offered by Treasury Secretary Andrew Mellon, one of the richest men in America, was “liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate,” as Herbert Hoover described Mellon’s argument in his own memoirs.

There’s reason to doubt that the relationship applies to today’s variety of inflation, which has been generated by factors such as pandemic-related supply chain obstacles and an aggressive expansion of corporate profits. The Phillips curve also depends on an accurate reading of unemployment.

As Ghilarducci observes, the published unemployment rate of 3.7% may be artificially low because it doesn’t account for workers who may still be kept out of the workforce by long COVID. As their illness abates, they may come flooding back into the workforce — a “large reserve army of labor,” as she calls it, indicating that the market isn’t nearly as tight as the Fed believes.

In any event, the fact that wage growth has lagged behind price inflation suggests that the first can’t be driving inflation higher — if anything, it’s holding inflation down.

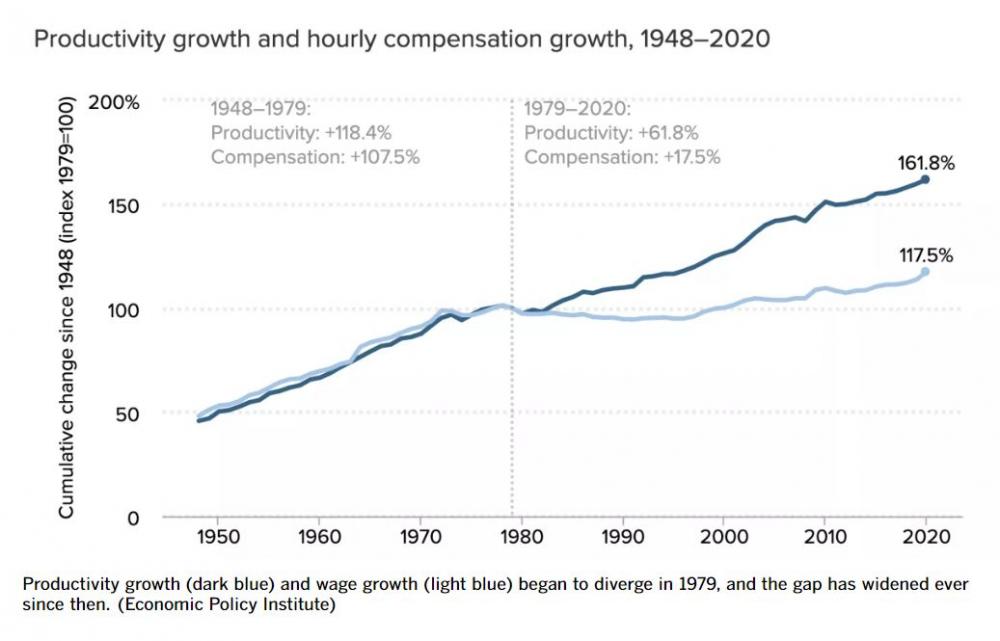

The inadequacy of wage growth is shown by two other factors. One is the disconnect between productivity growth and wage growth. The two factors marched along together from 1948 until 1979, as the labor-oriented Economic Policy Institute has shown. Since then, the gap between them has grown: From 1979 through 2020, U.S. productivity advanced by 61.8%, but average wages grew by only 17.5%.

The second factor is the value of the federal minimum wage, which peaked in 1970 at an inflation-adjusted $12.04 per hour (in 2022 dollars). Today it’s mired at $7.75, where it was set in 2009.

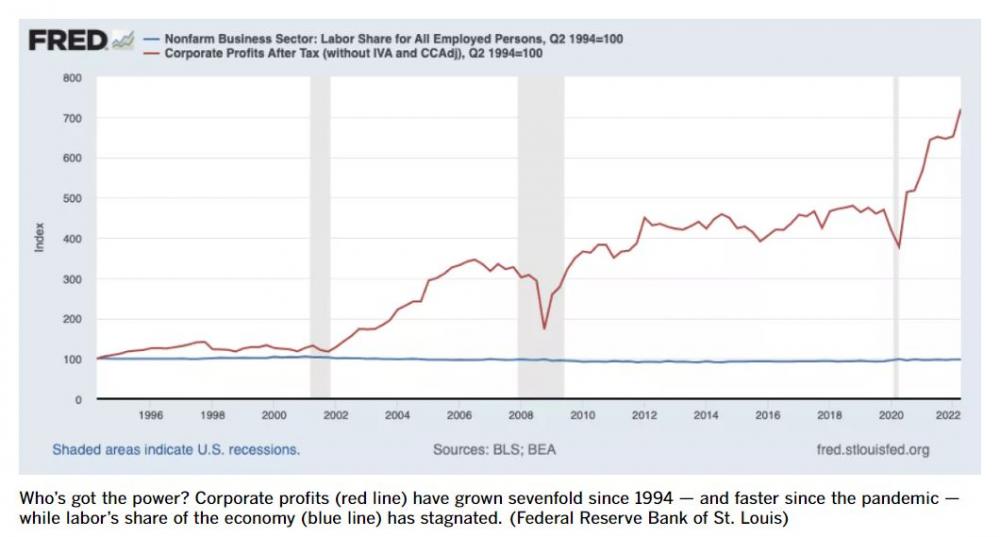

Another trend worth examining is labor’s share of national income compared with corporate profits (which are upstreamed to executives and shareholders). Since 1994, corporate profits have grown sevenfold while the labor share has been stagnant. Since the pandemic took hold in the first half of 2020, corporate profits have doubled while labor has lost ground.

It’s proper to note that white-collar workers gained significant freedoms as a result of the pandemic, including the health-giving ability to work from home, while the laboring class — those so-called essential workers — were forced to report to work at restaurants and retail stores, at great risk to their health. It’s those more privileged workers, however, who are now facing more pressure, even mandates, to work from the office and figuratively punch the clock.

The union activism that has brought representation to workers at 234 Starbucks locations in 36 states and the District of Columbia this year is certainly encouraging, but it’s a work in progress. The company owns 9,000 stores nationally. Moreover, the company has resisted cooperating on the crucial next step, which is negotiating contracts with those organized workers.

Thus far, negotiations have been underway at only three locations, although the company said Monday that it is willing to open negotiations next month at all the unionized stores.

The Starbucks victories are overshadowed by the long-term decline of union representation in the U.S., which continued through the pandemic. Union membership shrank in 2021 to 14 million, down by 241,000 from the year before, with the percentage of union-represented workers falling to 10.3%. In 1983, when the government started compiling statistics, the U.S. had 17.7 million unionized workers, 20.1% of the workforce.

As unions struggle to retain their collective strength, mergers among employers outpace them, reducing the options for workers seeking to move to new jobs and strengthening employers’ power.

The truth is that worker power can’t grow unless it’s abetted by government oversight. Regulation of labor and workplace safety practices has been stifled over the years.

“In recent years,” the Treasury Department observed in a March report, “the probability of a firm being inspected has decreased sharply.” The government’s Occupational Safety and Health Administration, for example, conducted 140,000 inspections in 1984; by 2019, the number had fallen to 81,000, and declined further during the pandemic.

Only recently, with new regulatory initiatives by the uniquely pro-union Biden administration, has oversight of working conditions and union organizing drives by the Department of Labor and the National Labor Relations Board improved.

Despite the reality on the ground, the Federal Reserve, which has more power than any other American institution to guide the course of the U.S. economy, is still wringing its hands over signs that demand for workers is “substantially exceeding the supply of available workers,” as Powell put it on Sept. 21. He took that as a sign that the labor market is so tight that wages will be forced higher.

The Fed’s medicine is aimed at reducing that imbalance by slowing the economy, thereby reducing demand for workers and thus the latter’s ability to recover the ground they have lost in an economy that has been wholly favorable to employers for some 40 years.

Powell says his aim is to “set the stage for achieving maximum employment and stable prices over the longer run.” Working people who are still struggling to fulfill the dream of a middle-class existence that has been the American promise since the 1940s might well wonder whether Dr. Powell’s cure will be worse than the disease.

[Los Angeles Times columnist Michael Hiltzik writes a daily blog appearing on latimes.com. His seventh book, “Iron Empires: Robber Barons, Railroads, and the Making of Modern America,” has just been published by Houghton Mifflin Harcourt. Follow him on Twitter at twitter.com/hiltzikm and on Facebook at facebook.com/hiltzik.]