The Trump administration is marketing its plan to give huge tax cuts to the richest U.S. households with a bold but fanciful claim: that these tax cuts will trickle down to help American workers by boosting economy-wide productivity and hence wages. The plan—the Unified Framework for Fixing Our Broken Tax Code—would (among other changes) reduce the statutory federal corporate tax rate from 35 percent to 20 percent. In a recent paper addressing the effect of the “Unified Framework” on wages of American workers, the administration’s Council of Economic Advisers asserts,

This analysis from the Council of Economic Advisers reviews the evidence that has driven other developed countries to pursue the path of lower corporate tax rates and estimates how business tax reform in the Unified Framework for Fixing Our Broken Tax Code (hereafter, the “Unified Framework”) is expected to affect wages for American workers.

Reducing the statutory federal corporate tax rate from 35 to 20 percent would … increase average household income in the United States by, very conservatively, $4,000 annually. The increases recur each year, and the estimated total value of corporate tax reform for the average U.S. household is therefore substantially higher than $4,000. (CEA 2017)

This claim is clearly wrong. Economic logic and evidence argues strongly that American workers should not expect any noticeable wage boost from cutting corporate income taxes. The main findings of this paper are:

- Since World War II, productivity and wage growth in the U.S. economy have been significantly greater in periods with higher corporate tax rates.

- There is essentially no robust relationship between post-tax profit rates and productivity-enhancing business investment in the U.S. economy. This weak relationship is why efforts to boost post-tax profit rates with tax cuts will likely do little to grow productivity.

- Even were productivity to grow, it would not necessarily lead to wage growth (i.e., productivity growth is a necessary, not a sufficient, condition for wage growth). In fact, in recent decades, the link between economy-wide productivity growth and wages of the vast majority of American workers has been almost entirely severed. In other words, pay and productivity used to rise tightly together but they no longer do.

- A steep corporate tax rate cut in 1986 did nothing to reverse the widening fissure between typical workers’ pay and productivity growth—a gap that was already apparent in that year. Another corporate cut today would likely again fail to reconnect pay and productivity.

- To support its claim that corporate tax cuts would boost wages, the CEA report cherry-picks findings from the research literature and also uses a highly misleading graph relating wage changes over just a few years to corporate tax rate levels. Claims that cutting corporate taxes will boost wages should examine a longer time horizon and focus on tax changes, not levels.

- The real key to boosting wage growth for the vast majority of American workers is restoring economic leverage and bargaining power that workers once had but which have been redistributed from workers to capital owners and corporate managers. Yet the Trump agenda has consistently pushed policies and rule changes that further weaken workers’ leverage.

Real-world data shows weak-at-best links between corporate tax cuts and wage growth

Bivens and Blair (2017) explain in detail how the theory for corporate tax cuts as a wage-boosting tool breaks down in the face of real-world data. This report provides a quick overview of this theory and then highlights how its predictions compare with real-world data.

The theory is the following: First, corporate income tax cuts boost post-tax profits, which then boost the returns to owning stocks or bonds. These higher returns induce households to spend less and save more, and this increased supply of savings pushes down the cost of borrowing, or interest rates. Lower interest rates then induce firms to borrow more to finance new plants and equipment, and this raises productivity by giving workers more and better tools to work with. Second, competitive labor markets force employers to reward workers for their productivity increases buy paying them higher wages.

This theory provides a number of empirical propositions regarding the effect of corporate tax changes on wage growth that can be tested with real-world data. The data show that many of the key predictions will almost surely fail.

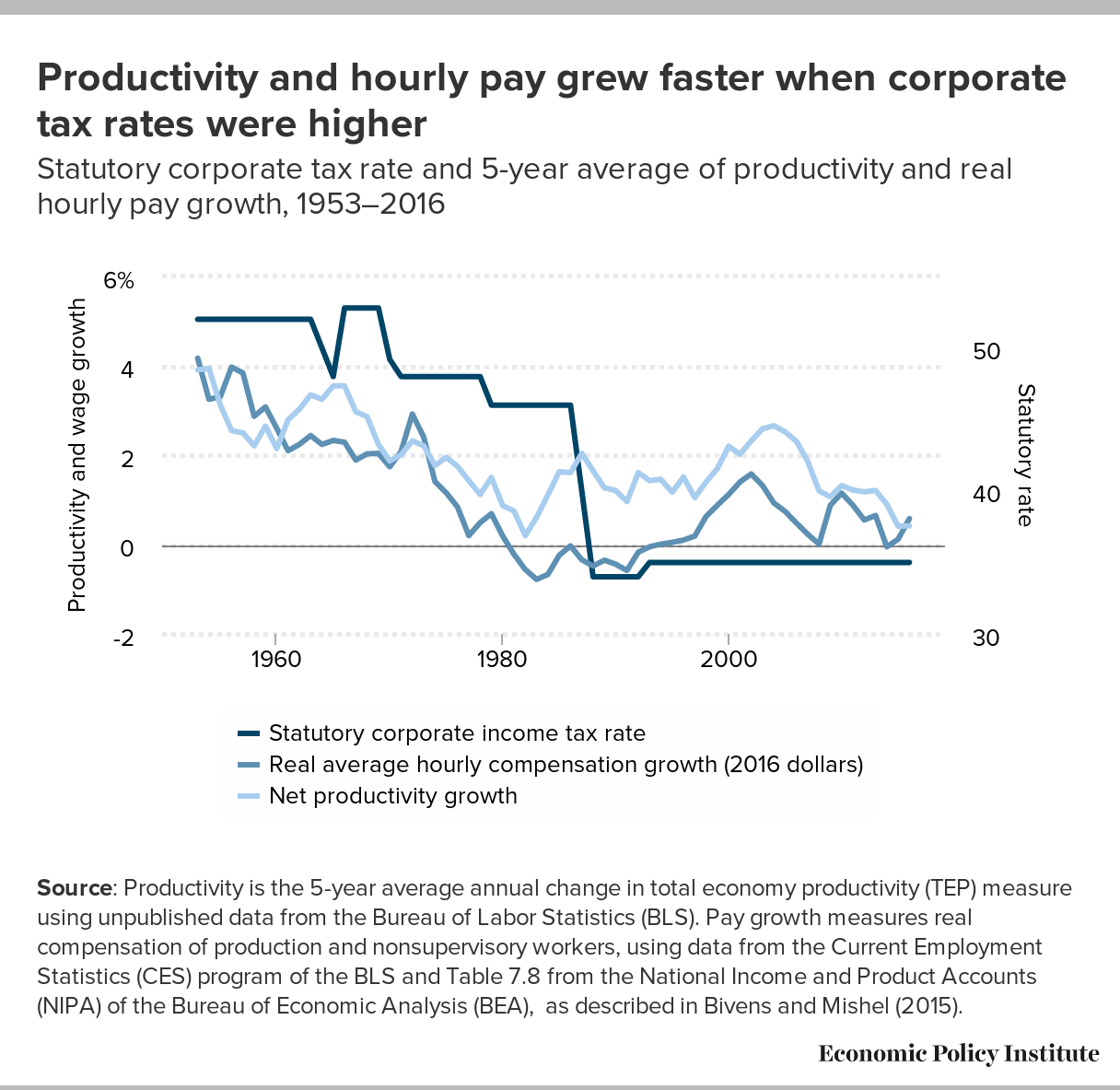

Before looking at the specific weak links in the causal chain, we review evidence relating to the overall claim that lower tax rates will boost productivity growth and wage growth. Figure A shows that at least since 1953, lower corporate rates (the dark line) have not noticeably boosted productivity growth and wage growth (the lighter lines). Both productivity and wage growth were substantially stronger in the first decades following World War II, when corporate tax rates were significantly higher than they were in the 1980s, 1990s, and 2000s.

This figure is also remarkable because it shows that the corporate tax rate was dramatically slashed in the late 1980s—precisely when “the relationship between corporate profits and worker compensation broke down,” according to the recent CEA (2017) report. As the report says,

Prior to 1990, worker wages rose by more than 1 percent for every 1 percent increase in corporate profits. From 1990–2016, the pass-through to workers was only 0.6 percent, and looking most recently, from 2008–2016, only 0.3 percent. The profits of U.S. multinationals are still American profits, but, increasingly, the benefit of those profits do not accrue to U.S. workers.

While it is true that the gains from overall economic growth of any kind have largely bypassed typical American workers since the late 1970s,1 Figure A and the CEA’s own statement discredit the claim that steeps cuts in corporate taxes would increase wages: If a steep corporate rate cut in the 1980s coincided with a damaging delinking of wages and profits then, why would another steep cut today reconnect wages and profits? As the rest of this report shows, it would not.

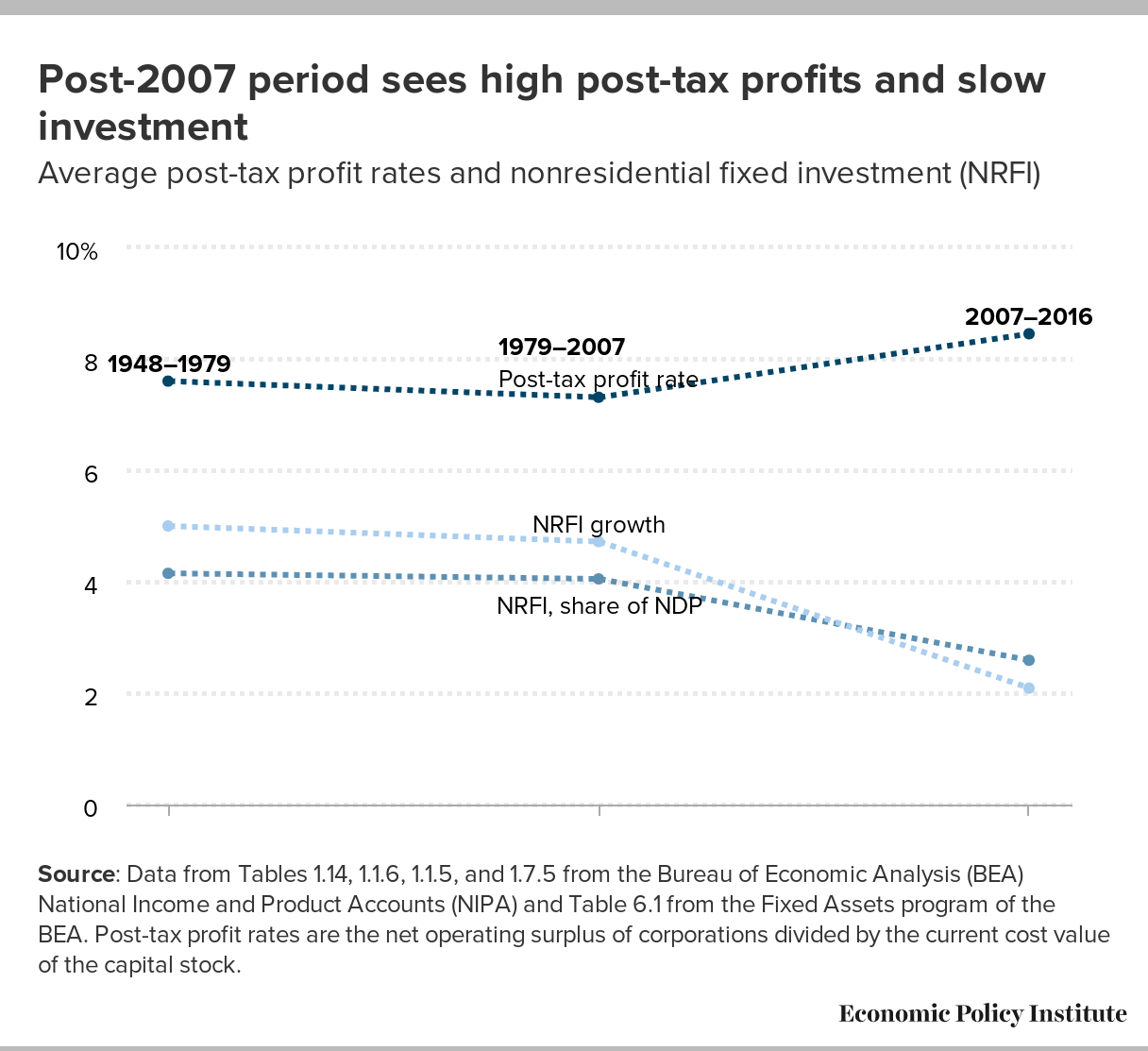

One reason that corporate tax rate cuts won’t boost productivity and thus wages is the weak association between post-tax profit rates and business investment. Remember, in theory, cutting corporate taxes is supposed to boost private-sector savings, with the increased savings leading to lower interest rates that encourage more businesses to invest in productivity-enhancing plants and equipment. But as Figure B shows, the link between profit rates and investment is historically weak, which weakens the entire “tax cuts boost productivity” argument.

The figure shows the post-tax profit rate, growth in nonresidential fixed investment (NRFI), and net NRFI (NFRI minus depreciation) as a share of total net domestic product (NDP) in three periods since 1948. While the post-tax profit rate is clearly higher in 2007–2016 than it was in earlier periods, NRFI growth is radically slower in 2007–2016. Some of this slowdown is simply due to slower economic growth overall post-2007, so the next set of bars scales NRFI as a share of NDP (NDP is gross domestic product minus depreciation). As the bars show, the post-2007 net NRFI share of NDP is notably lower than it was from 1948 to 2007.

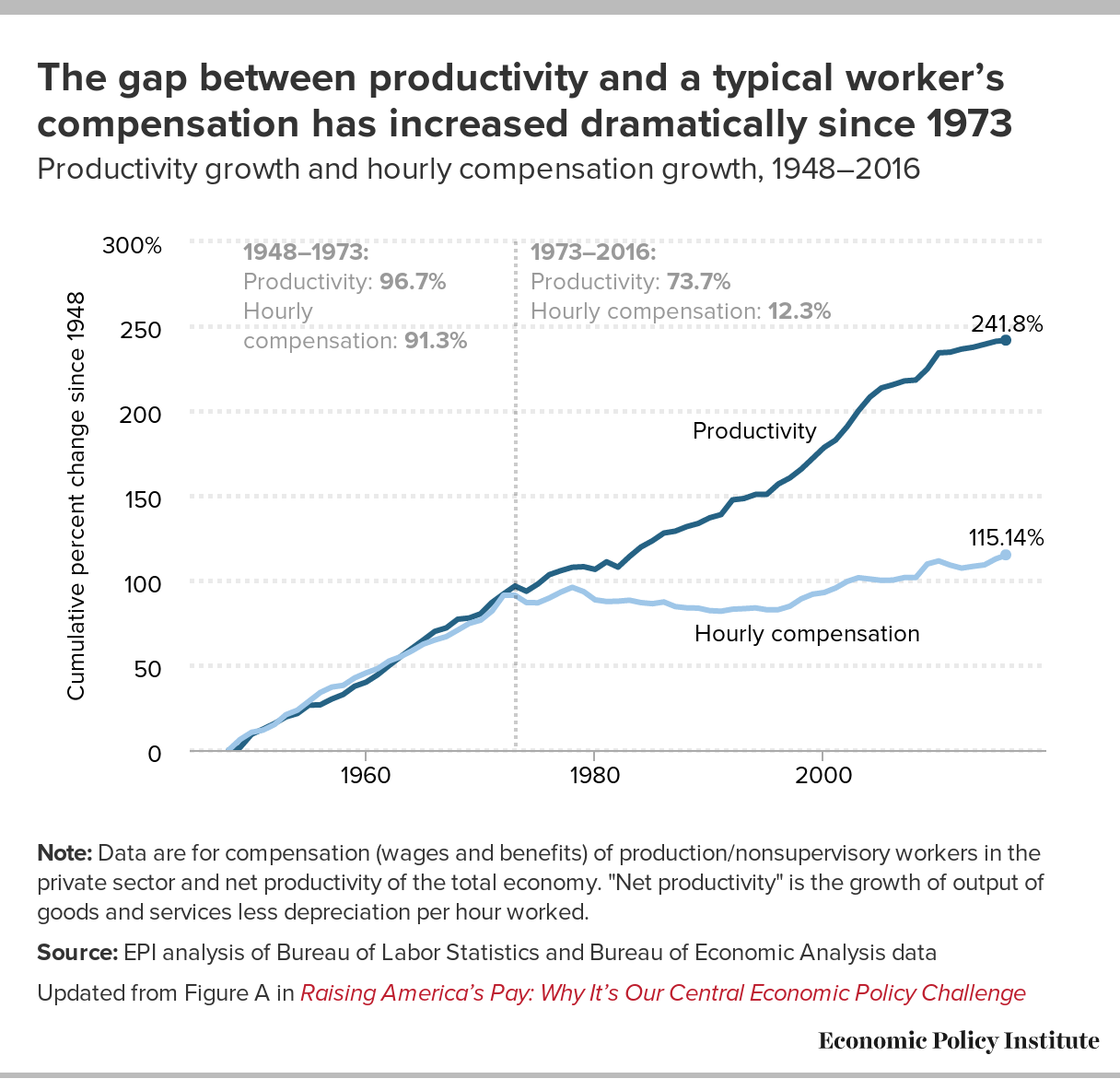

Finally, even if corporate rate cuts did boost savings, lower interest rates, and spur productivity growth through more capital investment, the benefits of all of these changes for typical American workers are still dubious. For decades the U. S. economy has seen a growing wedge between productivity growth and wage growth, meaning that pay and productivity used to rise tightly together but they no longer do, as shown in Figure C. Since the late 1970s, only about 10–15 percent of each 1 percentage-point increase in productivity growth has translated into higher hourly pay for typical American workers (see Bivens and Mishel 2015 for an overview of trends in pay and productivity).

There is very little reason to think that broad economic evidence indicating a historically weak payoff from cutting corporate taxes for American wage growth will be different in the future. First, many aspects of today’s economy further weaken the ability of corporate tax rate cuts to somehow unleash a new wave of economic growth that spurs wage growth. One aspect is the fact that the user cost of capital (i.e., interest rates) is already at historically rock-bottom rates and has created a savings glut. Rate cuts that reduce interest rates will therefore have very little purchase in today’s economy. Long-term interest rates have been historically low for a decade now, and much evidence indicates that powerful long-run structural influences will continue to hold long-term rates low in years to come.2 These structural influences have contributed to a glut of desired savings relative to planned investment. The excess supply of investable funds has predictably held down the price of these funds (interest rates).

The mirror image of this savings glut is a shortfall in aggregate demand (i.e., spending by households, businesses, and governments). This shortfall in aggregate demand has been the key constraint holding back American economic growth for at least the past eight years, if not longer. Corporate tax cuts are among the weakest fiscal policy tools available to spur demand growth because they benefit the highest-income households, who own the lion’s share of corporate stock in the American economy. Tax cuts aimed at lower- and working-class households are much more effective in spurring spending, because these families are far more likely than high-income households to spend (rather than save) an extra dollar they receive in tax cuts.3 Direct government spending (increased infrastructure spending, for example) is also far more effective than corporate tax cuts for boosting aggregate demand and spurring demand growth.

The CEA report provides no evidence that the historic nonrelationship between corporate taxes and wages will reverse in the future

In its recent report estimating large wage gains stemming from corporate tax cuts, the Trump administration’s Council of Economic Advisers (CEA 2017) claims that its conclusions are “driven by empirical patterns that are highly visible in the data, in addition to an extensive peer-reviewed research” (emphasis added).

The data do not show that corporate rate cuts boost wages

The claim that benefits of corporate tax cuts for boosting wages are “highly visible in the data” is clearly false. The figures earlier in this report confirm that there is essentially no visible relationship between corporate taxes, wages, and productivity. To buttress its claim, the CEA (2017) report provides a graph of wage growth from 2013 to 2016 for countries with the 10 highest and 10 lowest statutory corporate tax rates in the Organization of Economic Cooperation and Development (OECD), a group of mostly advanced economies. The graph (Figure 1 in the CEA report) shows that the unweighted average wage growth in the low-tax countries was significantly higher in 2015 and 2016 than the unweighted average wage growth in the higher-tax countries.4

It is deeply puzzling just what a graph that shows correlation is supposed to prove about causation. Most notably, there is no claim that corporate tax policy changed in those years and hence drove the higher wage growth in low-tax countries. Even the CEA itself implicitly confirms that corporate tax policy changes are the correct variable to assess, when later in its own report, it praises another study for assessing “long-run outcomes …[that should be] thought of as the recurring flow of income after the corporate tax changes have fully taken hold” (emphasis added). Showing a short-run graph that has results that are driven by corporate tax levels rather than changes completely fails to demonstrate that the benefits to wage growth of cutting corporate taxes are “clearly visible in the data.”

Using OECD data, we were able to essentially replicate the CEA results (data and figure available upon request; see Appendix). The most striking finding is that the fast wage growth of the “low-tax countries” in 2015 and 2016 is driven quite disproportionately by three small countries: Estonia (6.6 percent average wage growth in those years), Iceland (7.5 percent average wage growth), and Latvia (6.8 percent average wage growth). These three countries combined account for 30 percent of the unweighted “low-tax” sample but well over half of the wage growth in the low-tax group, yet their GDPs combined represent less than 0.4 percent of U.S. GDP.

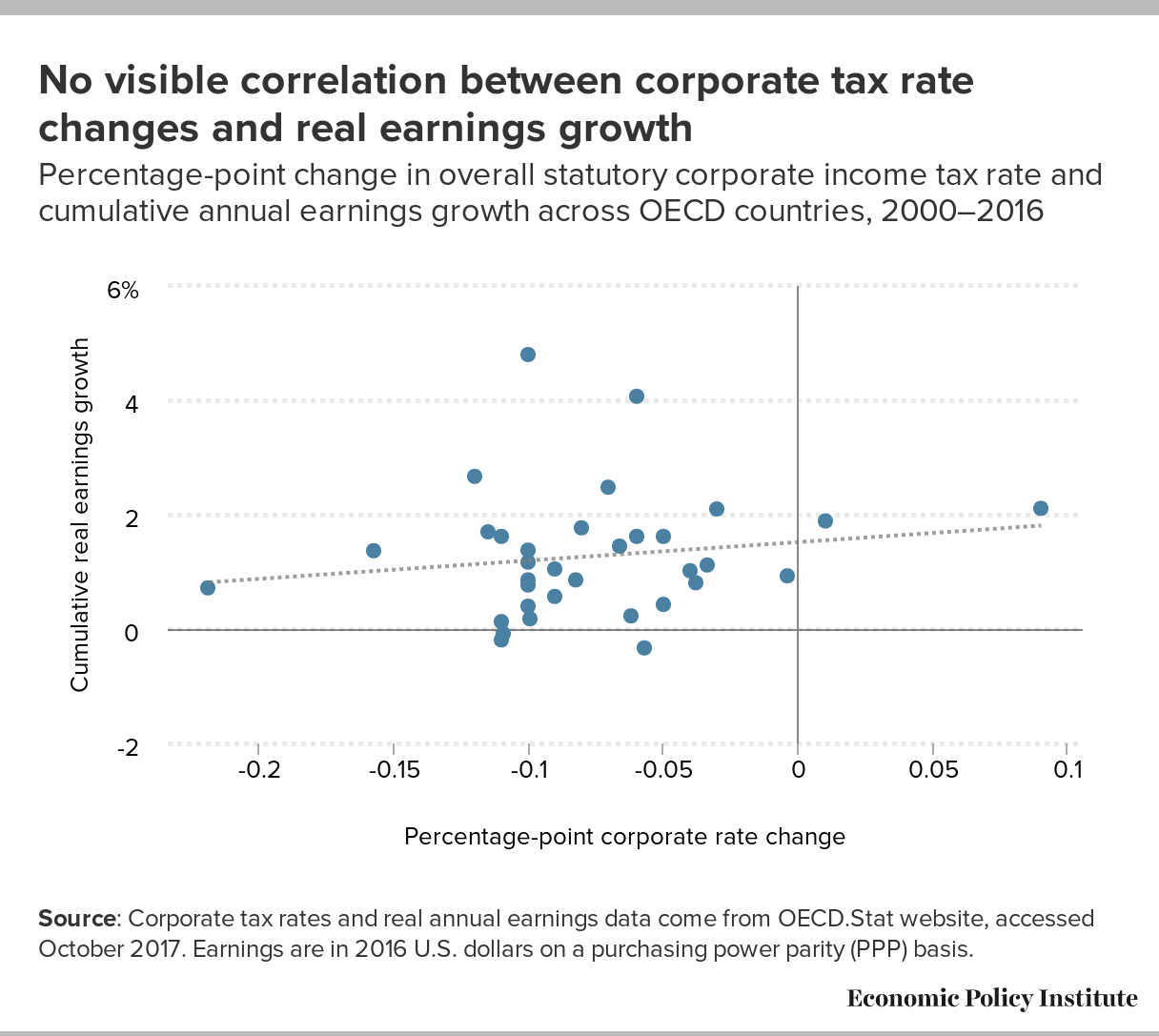

Finally, we use this same OECD data to show changes in corporate tax rates and cumulative wage growth from 2000 to 2016 (see Figure D). This longer-run view of the effect of corporate rate changes on wage growth is much more relevant for testing theoretical predictions about changing corporate rates and wages. This figure shows that there is no obvious correlation between corporate rate changes and wages; again the beneficial effect of cutting corporate taxes on wages is absolutely not “highly visible in the data.” In fact, the simple slope of the line through the scatterplot is positive, indicating that steeper cuts in corporate rates (the farther to the left of zero) were associated with slower wage growth (slightly and insignificantly, to be sure, as rate cuts just don’t affect wages much).

The authors misrepresent research findings on corporate tax rates and wages

After failing to demonstrate clear evidence of a strong link between corporate tax changes and wages, CEA (2017) provides a clearly cherry-picked review of the academic research to claim that most economic evidence shows that the bulk of corporate tax cuts would raise wages. This claim is obviously untrue; most researchers who have studied corporate taxes and wages believe that the benefits of corporate rate cuts will accrue more heavily to capital incomes than to wages because the “incidence” of a corporate tax—where its economic burden is felt—falls more heavily on capital incomes than on wages.5 This clear majority view is why organizations that have a professional obligation to accurately forecast economic and revenue trends—organizations such as the Congressional Budget Office (CBO), the Department of Treasury Office of Tax Analysis (OTA), and the Tax Policy Center (TPC)—all allocate the vast majority (from 75–80 percent) of the incidence of corporate taxes to capital incomes, not wages.

A full literature survey including the studies cited by the CEA (2017) is provided in Gravelle (2017). It is clear from Gravelle’s comprehensive review that CEA (2017) has been extremely selective regarding which studies from the literature to cite, highlighting only those that provide large estimates of wage gains from corporate tax cuts and ignoring the clear fact that these studies are by and large lower-quality than studies finding much smaller wage effects.

While a blow-by-blow review of the professional debate over the robustness of regression results is beyond the scope of this report, it is possible to identify two examples of how the CEA inappropriately characterized some of the studies that it claims support its policy.

First, CEA 2017 cites estimates of large economic gains stemming from tax reform made by Auerbach, Kotlikoff, and Koehler (AKK, henceforth) (2017). But AKK 2017 actually assessed a previous tax proposal (the Congressional Republican “Better Way” plan). Crucially, the element of the previous proposal that drives the large economic gains in AKK (2017) is not included in the “Unified Framework.”6 Hence citing AKK (2017) in the current debate is actively misleading.

Second, CEA 2017 cites numerous papers in support of the proposition that firms share “rents” (excess profits) with workers, and claim from this that anything that boosts firms’ profits (like cutting corporate tax rates) will hence boost wages. But profit rates have been historically high in recent years, and yet wage growth remains low, largely because workers’ leverage in claiming such excess profits has been severely eroded by a range of nontax policy choices.7

And as we noted earlier in this report, the introduction to the CEA 2017 paper highlights the breakdown in the relationship between increased profits and wage growth—with this breakdown coming exactly during a time when corporate tax rates were significantly reduced.

In the CEA report, improving “competitiveness” through corporate tax cuts means increasing the trade deficit

For corporate tax cuts to produce very large wage increases, a key assumption would have to hold. In theoretical models, corporate rate cuts have the potential to boost wages only when flows of international capital respond incredibly robustly to any small change in American interest rates.8 In the jargon, this is assuming that the U.S. is a “small, open economy” and its wages, prices, and interest rates are wholly set on global, not domestic, markets. Were this extreme “open economy” assumption correct, as corporate rates are cut and post-tax profits rise, an enormous flood of savings from abroad would enter the U.S. economy and be put into productive capital investments. This inflow would continue until a rising capital stock pushes down pre-tax profit rates enough to move post-tax profit rates back towards global averages.9

There are three issues that are important to flag about this process. First, the U.S. is not a small, open economy, and domestic influences matter greatly to domestic prices, wages and interest rates.

Second, an inflow of capital into the United States requires we run a larger trade deficit. Claims are often made that cutting corporate tax rates will improve the “competitiveness” of the U.S. economy. To the degree that “competitiveness” has any economic meaning at all for most laypersons, it likely means the United States having more balanced trade, not larger trade deficits.10 Larger trade deficits would displace jobs from the manufacturing sector disproportionately, an outcome that would seem to be at odds with Trump administration promises to revive this sector.

Third, over time, a larger trade deficit and inflow of foreign savings implies a steady transfer of ownership of American assets to foreigners. Again, it seems odd to claim that American “competitiveness” would be improved by a policy that handed American assets to foreign investors to finance an excess of imports over exports.

CEA report misrepresents the problems of “profit-shifting”

Finally, the CEA (2017) claims that allegedly high U.S. corporate tax rates have led to profit-shifting abroad.11 The authors write, “In general, profits earned abroad evidence the willingness of U.S. firms to invest in production and business operations overseas, at the expense of domestic investment.”

This is clearly wrong. The bulk of high-quality evidence on the very real problem of profit-shifting indicates that actual investment and employment is not shifting abroad due to tax differentials. Instead financial engineering is making profits appear to have been earned abroad, so that business owners can maximize the benefits of having profits appear in tax havens.12 Nobody really thinks the Cayman Islands is a global manufacturing powerhouse, yet a stunning share of the world’s profits are booked there through financial and accounting engineering. CEA (2017) notes studies showing that this profit-shifting of obviously fictitious economic activity has led to mismeasurement of economic activity occurring within the United States; accounting for this profit-shifting shows that GDP in the United States is larger than our national accounts currently indicate, by roughly 2 percent.13 Yet the CEA (2017) misleads readers into thinking that ending profit-shifting would actually increase U.S. GDP and create jobs, rather than just solve a measurement problem.14

To clarify the difference between activity and measurement of that activity, imagine that you have an hour to drive 60 miles. For the first 30 minutes your speedometer registers 50 miles per hour with the accelerator floored. You despair of reaching your destination in time. Then your mechanic friend traveling with you notices something wrong with your speedometer and bangs on the dashboard to fix it. Now with the accelerator floored your speedometer registers 70 miles per hour. Your actual speed hasn’t increased. You would have made it to your destination well in time regardless of what your speedometer was telling you. Better measurement is nice, but it has not made the car go any faster. One imagines that the authors of the CEA report know that promises of faster growth in this context are deeply misleading, yet they make them anyway.

The fact that profit-shifting is about accounting tricks rather than real economic trends is affirmed in the CEA’s own report, in Figure 3 (CEA 2017), which shows the percent of overseas profits of U.S.-based multinationals held abroad. The share declines precipitously in 2004, falling by 20 percentage points (roughly a third). Was there a flood of factory “insourcing” in 2004? No, but there was a one-year “repatriation holiday” that allowed firms to repatriate profits held abroad at a preferential tax rate. The response was totally predictable—profits flowed quickly home and yet job and GDP growth barely registered.15

Conclusion

Mishel and Eisenbrey (2015) highlight a number of policies to tackle slow wage growth. They also usefully distinguish between policies that would work and those that wouldn’t. Corporate tax rate cuts absolutely belong on the list of fake solutions to the slow wage growth bedeviling typical American workers.

The urge to market corporate tax cuts as wage boosters makes a lot of sense. Americans want faster wage growth and want policymakers to get credit for taking these desires seriously. There is enough in economics textbooks to make the link between corporate rate cuts and wage increases theoretically plausible. But the real-world data couldn’t be clearer: a strategy to boost wages based on cutting the taxes paid by corporations is ridiculous policy. Policymakers who are sincere about boosting wages would heed the advice of Mishel and Eisenbrey (2015), and undertake policy measures to redistribute economic leverage and bargaining power away from capital owners and corporate managers and back to low- and middle-wage workers.

The Trump administration has so far done worse than ignore this insight about leverage and bargaining power. Trump and his team have instead tried along multiple dimensions to continue to redistribute economic power from typical workers to capital-owners and corporate managers, as documented in EPI (2017). Given that the administration has weighed in so heavily against workers in policy fights over the past year, it’s not surprising to find it pushing a tax plan that would provide nothing for these workers, either.

Appendix 1: Replicating CEA (2017) Figure 1

As noted in the text, CEA (2017) shows wage growth from 2013 to 2016 for two groups of OECD countries: those with the 10 highest and 10 lowest statutory corporate tax rates.16 Given that it is such a short period and that no corporate rate changes are identified, it is essentially a near-worthless graph. Nevertheless, we replicated it just to examine what could be driving the results (results are available upon request). What we found is reported in this EPI paper: the results are largely driven by three very small economies that happened to have fast wage growth in 2015 and 2016.

Since the CEA does not identify them, we provide the list of the highest and lowest statutory tax rates below.

The countries with the lowest averages rates from 2012 to 2016, ranked from lowest to highest, are Ireland, Latvia, Slovenia, the Czech Republic, Hungary, Poland, Iceland, Turkey, Estonia, and the United Kingdom.17 Because Turkey does not have earnings data through 2016, we instead used the country with the next-lowest rate on the list: Finland.

For both 2012–2016 and 2013–2016, the 10 highest statutory corporate tax rates in the OECD are in Luxembourg, Australia, Mexico, Germany, Portugal, Italy, Belgium, Japan, France, and the United States.

About the author

Josh Bivens joined the Economic Policy Institute in 2002 and is currently the director of research. His primary areas of research include macroeconomics, social insurance, and globalization. He has authored or co-authored three books (including The State of Working America, 12th Edition) while working at EPI, edited another, and has written numerous research papers, including for academic journals. He often appears in media outlets to offer economic commentary and has testified before the U.S. Congress. He earned his Ph.D. from The New School for Social Research.

Endnotes

1. A shift from wages to profits is just one channel through which economic growth can bypass typical workers’ wages. Another channel is redistribution within the wage “bill” that companies pay for all their workers—CEOs’ salaries exploding while typical workers’ pay stagnates, for example. Much research, such as Bivens and Mishel (2015), highlights that this within-wage-bill redistribution has been the single-biggest factor in driving growing inequality in recent decades, and that its role was particularly large in the 1980s.

2. See Rachel and Smith (2015) for evidence on these secular trends in global interest rates.

3. See Table 1 in Bivens and Blair (2017) for this ranking of fiscal policy changes by their effect in spurring growth in aggregate demand.

4. The authors provide essentially no documentation in their report for this figure. In the appendix we are able to very closely match the figure using data from the Organization of Economic Cooperation and Development (OECD), but due to the nonexistent data documentation in their report, very slight differences between our graph and theirs might remain.

5. For example, sales taxes can be officially levied on makers of cigarettes, but it is almost surely the case that consumers of cigarettes would end up bearing the burden (“incidence”) of such a tax, as prices of cigarettes rise to pass on the value of the tax.

6. Specifically, the feature of the “Better Way” plan that drove the findings in Auerbach, Kotlikoff, and Koehler (AKK 2017) was the “destination-based cash-flow tax” (DBCFT) as a replacement for the current corporate income tax. The “Unified Framework” does not include a DBCFT and only includes cuts to rates of the current corporate income tax.

7. For a discussion of some of these policy choices, see Bivens et al. (2014).

8. See Gravelle (2017) for the various other assumptions that can affect the incidence of corporate income tax rates.

9. The standard assumption in macroeconomics is that as the size of a nation’s capital stock rises, the marginal return to each increment of capital investment falls, pushing down the profit rate.

10. Bivens and Blair (2017) provide a relatively thorough overview of the economics of corporate tax cuts and claims regarding “competitiveness.”

11. See Bivens and Blair (2017) for why U.S. effective rates are actually not particularly out-of-line with advanced country peers.

12. See Clausing (2016) and Zucman (2014) for evidence on this profit-shifting stemming from accounting engineering.

13. See Guvenen et al. (2017) for this estimate and its derivation.

14. To be clear, much about globalization and the ability to substitute foreign production for U.S. production has harmed American workers. But this process has not been driven by tax rates.

15. See Huang and Marr (2014) for a good review of the evidence on the economic effects of the 2004 repatriation holiday.

16. As always, it is worth noting that statutory rates and effective rates (or what corporations actually pay after loopholes and deductions are used) can be very different. As Bivens and Blair (2017) have noted, the U.S. effective rate is much closer to international norms than its statutory rate.

17. CEA (2017) is not totally clear whether its analysis looks at 2012–2016 or 2013–2016 averages for corporate tax rates. The report says, “Between 2012 and 2016…”, but the data in Figure 1 begins in 2013. If we instead calculate countries’ tax rates between 2013 and 2016, the United Kingdom drops out and is replaced by Switzerland. No real change results to the wage growth figures.

References

Auerbach, Alan, Lawrence Kotlikoff, and Darryl Koehler (AKK). 2017. Assessing the House Republicans’ “A Better Way” Tax Reform.

Bivens, Josh, and Hunter Blair. 2017. Competitive Distractions: Cutting Corporate Tax Rates Will Not Create Jobs or Boost Incomes for the Vast Majority of American Families. Economic Policy Institute.

Bivens, Josh, Elise Gould, Lawrence Mishel, and Heidi Shierholz. 2014. Raising America’s Pay: Why It’s Our Central Economic Policy Challenge. Economic Policy Institute.

Bivens, Josh, and Lawrence Mishel. 2015. Understanding the Historic Divergence Between Productivity and Typical Workers’ Pay: Why It Matters and Why It’s Real. Economic Policy Institute.

Council of Economic Advisers (CEA). 2017. Corporate Tax Reform and Wages: Theory and Evidence.

Bureau of Economic Analysis. Various years. National Income and Product Accounts Interactive Data. Accessed October 2017.

Bureau of Economic Analysis. Various years. Fixed Assets Interactive Data. Accessed October 2017.

Bureau of Labor Statistics (U.S. Department of Labor) Current Employment Statistics program. Various years. [Interactive tables].

Clausing, Kimberly. 2016. The Effect of Profit Shifting on the Corporate Tax Base in the United States and Beyond.

Gravelle, Jane. 2017. Corporate Tax Reform: Issues for Congress. Congressional Research Service.

Guvenen, Fatih, Raymond Mataloni Jr., Dylan Rassier, and Kim Ruhl. 2017. Offshore Profit Shifting and Domestic Productivity Measurement. National Bureau of Economic Research (NBER) Working Paper No. 23324.

Huang, Chye-Ching, and Chuck Marr. 2014. Repatriation Tax Holiday Would Lose Revenue and Is a Proven Policy Failure. Center on Budget and Policy Priorities.

Mishel, Lawrence, and Ross Eisenbrey. 2015. How to Raise Wages: Policies That Work and Policies That Don’t. Economic Policy Institute.

Organization for Economic Cooperation and Development (OECD). Various years. OECD.Stat interactive database. Statutory corporate tax rates. Accessed October 2017.

Organization for Economic Cooperation and Development (OECD). Various years. OECD.Stat interactive database. Average annual wages. Accessed October 2017.

Rachel, Lukasz, and Thomas Smith. 2015. Secular Drivers of the Global Real Interest Rate. Working Paper, Bank of England.

Zucman, Gabriel. 2014. “Taxing Across Borders: Tracking Personal Wealth and Corporate Profits.” Journal of Economic Perspectives, vol. 28, no. 4, 121–148.

Spread the word