A proposal in the Biden-Harris Administration’s 2025 budget would require households with more than $100 million in wealth to pay income taxes of at least 25 percent of their annual income, including their unrealized capital gains — gains in the value of assets that they have not yet sold. Critics argue that unrealized capital gains, which are a primary source of income for many extremely wealthy households, are mere “paper” gains that do not constitute real income (though they meet a textbook definition of income). But unrealized gains make asset owners better off in very real ways. Claiming that unrealized gains are not “real” is akin to claiming that individuals such as Jeff Bezos and Elon Musk are not rich unless they sell their companies’ stock.

Critics also claim the proposal would mark a radical departure from current tax practices, but this too is incorrect. Two of the main types of assets that middle-income households own — their homes and defined-contribution retirement accounts like 401(k)s — are already taxed in ways that resemble proposals to tax the unrealized capital gains of the very wealthy. A family’s property taxes typically rise as the value of their home rises, and middle-class people pay the tax year after year in amounts reflecting those gains without selling their homes. Retirement account holders are required to begin realizing their deferred gains in those accounts and pay the associated tax when they reach a certain age, and their heirs then pay tax on any remaining gains.

Homes and retirement accounts account for relatively small shares of the income and wealth of very wealthy households, who tend to directly own large amounts of corporate stock or other capital assets. These assets face no comparable required realization requirement or annual tax. Instead they often increase in value, tax-free, year after year, and if they are never sold, the income tax that would be owed on those gains is simply erased when their heirs inherit them.

Requiring very wealthy people to pay income taxes on their unrealized gains and ending their ability to permanently avoid income tax when they pass appreciated assets to their heirs would thus constitute a reasonable reform. It would make the tax code more equitable while raising $500 billion in revenue over ten years, according to the Treasury Department, from a small subset of the wealthiest households in the country.

Substantial Income of Very Wealthy Households Escapes Annual Tax

The individual income tax is our main federal tax, accounting for roughly half of federal revenue. For households along most of the income spectrum, the progressive federal income tax generally works as it should, with higher-income households paying a larger share of their incomes in tax than households with lower incomes. But this relationship often breaks down at the very top. That’s because very wealthy households accumulate a very large share of capital gains (increases in the value of stocks, bonds, real estate, or other assets), which enjoy two important tax advantages: deferral of unrealized capital gains and stepped-up basis.

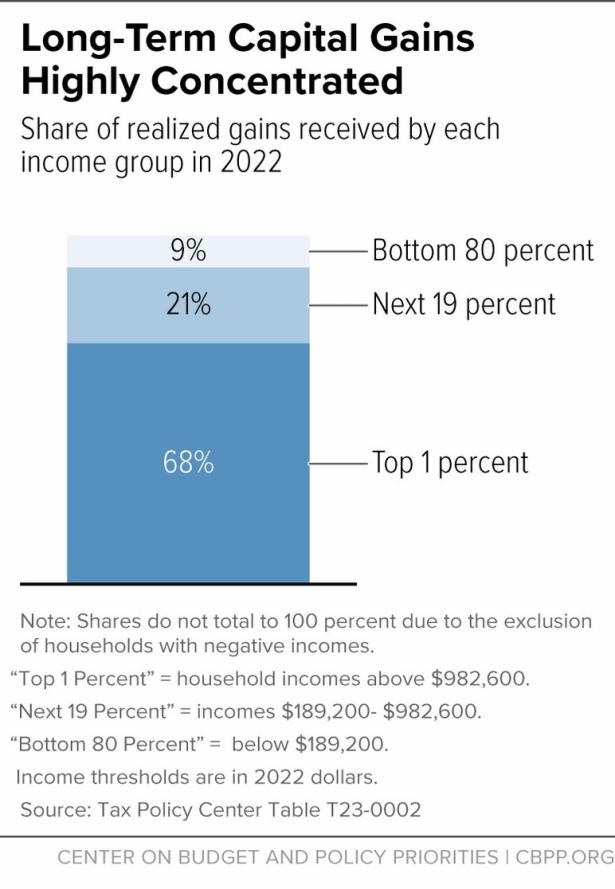

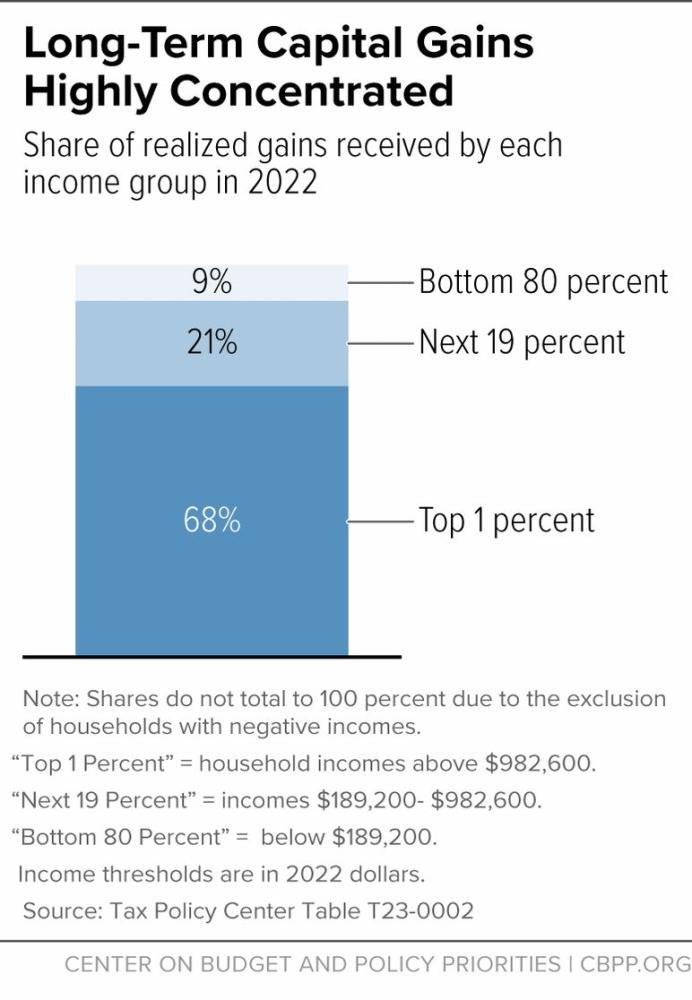

Figure 1

Deferral of capital gains income. Households that accumulate capital gains don’t have to pay tax on those gains until, or unless, they “realize” these gains, usually by selling the asset. This ability to put off paying capital gains tax is known as “deferral.” Deferral overwhelmingly benefits wealthy households because they own the overwhelming share of capital gains: nearly 70 percent of realized capital gains go to the top 1 percent of taxpayers. (See Figure 1.)

The distribution of unrealized gains is also highly skewed toward the very wealthy. Because of deferral, wealthy households only report a small share of their total capital income on their tax returns. Unrealized gains aren’t taxed, so filers don’t have to report them.

Research shows that unrealized gains constitute a growing share of a household’s total income as one moves up the wealth scale. In 2021, for example, the Washington Post noted that “the wealth of nine of the country’s top [tech industry] titans has increased by more than $360 billion in the past year,” and nearly all of the increase was due to the rising value of their holdings of their companies’ stock. Without policy changes, much of this wealth increase might never appear on income tax returns.

Stepped-up basis. Under a tax code provision known as “stepped-up basis,” the income tax that a wealthy person would have owed on an asset’s increase in value since they purchased it is erased when they die and pass their appreciated asset to their heirs. Neither they nor their heirs owe any income tax on this increase. (Technically, the asset’s basis — or the price paid for it — is “stepped up” to its fair market value at the time of inheritance.) Stepped-up basis encourages wealthy people to turn as much of their income into capital gains as possible and hold assets until their death, when a lifetime of gains becomes permanently exempt from income tax.

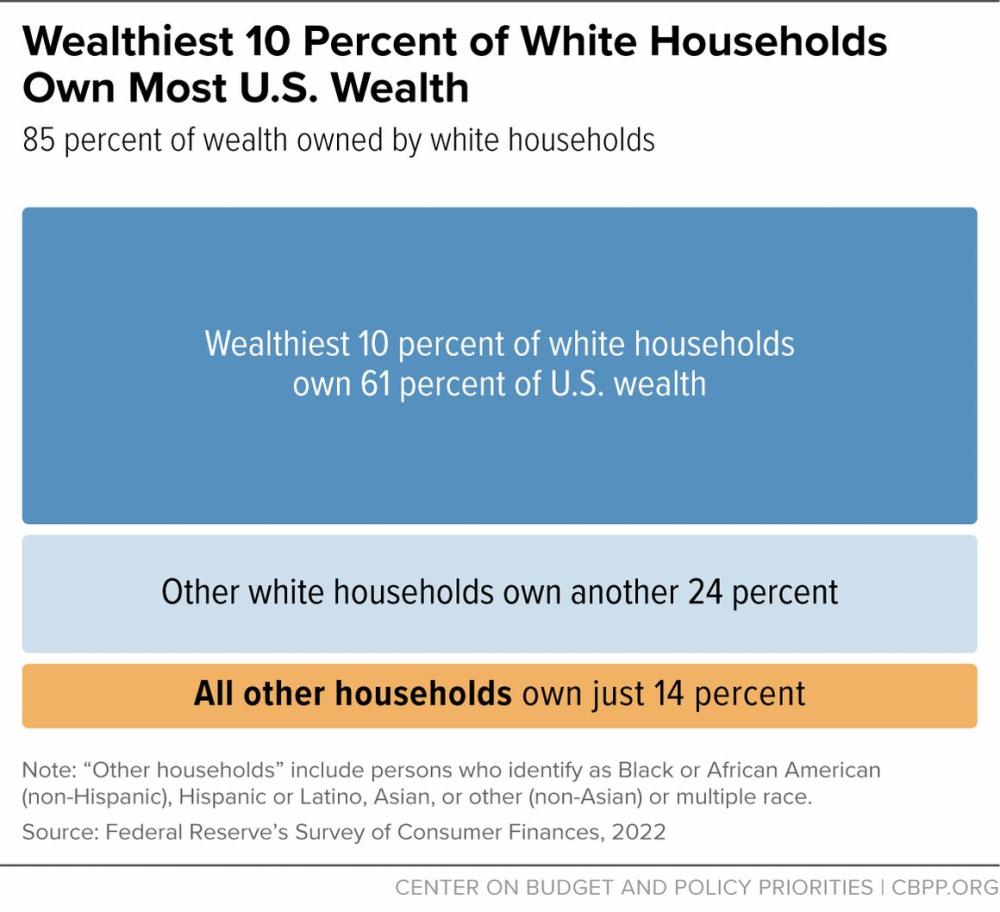

Together, deferral and stepped-up basis enable some of the country’s wealthiest people to go through life without paying income taxes on much or all of their income each year, or ever. Among other impacts, this worsens inequality in income and wealth, both overall and across racial and ethnic groups. Because of racial barriers to economic opportunity, households of color are overrepresented at the lower end of the income and wealth distributions, while white households are overrepresented among the wealthy. For example, the wealthiest 10 percent of white households — a group that makes up just 7 percent of households — holds 61 percent of the nation’s wealth. By contrast, people of color account for 33 percent of all households but just 14 percent of the nation’s wealth. (See Figure 2.)

Figure 2

Policymakers can change the tax code in several ways to treat some or all of the unrealized capital gains of the wealthiest households as taxable income. One is to make the gains taxable each year, as in Senate Finance Committee Chairman Ron Wyden’s proposal to shift to a “mark-to-market” system for taxing capital gains. A much more modest approach would be to repeal stepped-up basis: while wealthy people could still avoid tax on unrealized capital gains throughout their lives, they would have to pay taxes on those deferred capital gains at death. A third option, which the Biden-Harris Administration has proposed, would combine elements of both by essentially requiring very wealthy households to prepay some of their taxes on unrealized capital gains each year — similar to the withholding system that applies to wages and salaries — and paying any remainder when those gains are realized.

Biden-Harris Proposal Would Eliminate This Tax-Free Treatment

The Biden-Harris Administration’s 2025 budget would establish a minimum tax on total income, including unrealized capital gains, for the 0.01 percent of households with at least $100 million in assets — the tax would phase in and apply fully to households with at least $200 million in wealth. The proposal would also end the stepped-up basis loophole for wealthy households with significant unrealized gains: married couples with at least $10 million in unrealized capital gains or single filers with at last $5 million in capital gains.

The proposal’s critics argue that unrealized gains do not constitute “real” income because the asset owner has not received cash in exchange for the asset, whose value can either rise or fall before the asset is sold. For example, a Heritage Foundation economist recently argued that “until an asset is actually sold, any increase in value is purely speculative. It isn’t real, hence the classification of unrealized.” But this argument ignores the fact that the wealthy receive significant new value — or income — from their assets even before they sell. Unrealized gains make asset owners better off in very real ways: stock purchased 20 years ago for $20 million that’s now worth $100 million has the same value as $100 million of stock purchased today (that has no unrealized gains yet).

As Martin Sullivan, chief economist at Tax Analysts, has explained, “nrealized gain is economic income. Unrealized does not mean unreal. The wealthy can see it very clearly on their brokerage statements, even if the IRS will not see it on tax returns.”

In addition to watching their untaxed income grow, wealthy households can use this income to finance their (often lavish) lifestyles. “It is a simple fact that billionaires in America can live very extraordinarily well completely tax-free off their wealth,” law professor Edward J. McCaffery writes. They can do so by borrowing large sums against their unrealized capital gains, without generating taxable income.

For example, Larry Ellison, Oracle’s chief executive officer and one of the world’s richest people, has pledged over 300 million shares of Oracle stock worth over $45 billion as collateral for a personal credit line. This lets him obtain cash without selling shares; thus, he avoids paying taxes, and the stock can continue growing in value. Though he must pay interest on the debt and he or his heirs will eventually pay back amounts borrowed (e.g., using the proceeds of appreciated assets that were never subject to the income tax), this is often a much cheaper strategy than selling stock and paying capital gains taxes. As a recent article by two tax scholars observes, “Ellison hasn’t just gotten richer on paper when he borrows against his stock to buy a Hawaiian island; he’s used that income just as if he’d sold the stock.”

This doesn’t mean that the gains only become income when they are leveraged to finance other investments or consumption. Quite to the contrary: the gains were always real income available to the filer to use to buy Hawaiian islands, yachts, or invest in other types of stock or business investments. The gains raise their purchasing power, making them better off, whether or not they use that purchasing power to actually purchase things.

Middle-Class People Often Taxed on Unrealized Gains or Required to Realize Gains

Critics of proposals to tax unrealized gains of wealthy people fail to acknowledge that two of the primary assets owned by non-wealthy people — their homes and defined-contribution retirement accounts like 401(k)s — are already taxed in ways that resemble the capital gains proposals. To be sure, there are important differences between the taxation of these types of assets and capital assets like directly held corporate stock; for example, property taxes are not income taxes and are applied by state and local governments, not the federal government. But as explained below, the reality is that in certain long-standing and uncontroversial contexts, asset owners pay tax as their assets gain value over time or are required to realize gains at a certain age. This fact contradicts critics’ claim that taxing unrealized capital gains would be novel or untested.

Property Taxes Apply to Unrealized Gains From Increases in Home Values

Corporate stocks and privately held businesses are the largest appreciable assets for the wealthiest people, but for the middle class, the biggest asset by far is their home. These homes are subject to annual state and local property taxes across the country. The methods of assessing property values and calculating taxes differ, but generally the tax is calculated by multiplying the assessed value of the property (minus any exemptions) by the local property tax rate. When a family buys a house, the property’s initial assessed value may be based on the purchase price of the house, and jurisdictions typically reassess the home’s value (based on what the house would sell for in a third-party transaction, for example) at specified intervals. As officials from the state of Illinois explained in a recent Q & A for residents:

Your property’s value is determined by many factors. Your assessment can increase because your neighborhood is improving, the sales prices of homes in your area are increasing, and inflation. The value that the assessor assigns to your property is the amount that the assessor determines your property would sell for in today’s market.

In a recent example from the end of last year, the state of Maryland announced that assessments for a segment of properties would rise 23.4 percent from the last assessment three years prior.

A home’s assessed value often increases over time due to market factors, and if it does, the property tax is partially a tax on the home’s increase in value, or an unrealized gain. This is the case even though no sale has occurred, and no cash has flowed to the homeowner. Yet the taxation of the portion of a property’s value that represents unrealized gains is a relatively uncontroversial aspect of a tax that accounts for over 15 percent of state and local general revenue, helping to fund public schools, for example.

If middle-income homeowners can pay taxes that in part reflect the increase in value of their primary asset, very wealthy households can pay income tax on the increase in value of their primary assets: corporate stocks.

Retirement Account Holders Must Pay Income Tax on Accrued Gains

Middle-class families who own corporate stocks typically do so within retirement accounts such as 401(k) accounts, rather than in private brokerage accounts. Families between the 60th and 80th income percentiles have 28 percent of their assets in retirement accounts but only 12 percent in directly held corporate stock. The situation is reversed for the top 1 percent of families: only 5 percent of their assets are in retirement accounts, versus 44 percent in corporate stocks.

Under a typical 401(k), a person sets aside an average of about $5,000 per year from their paychecks on a pre-tax basis. The underlying assets typically increase in value over time, and account holders do not pay tax each year on their gains. Thus, owners of retirement accounts, like direct owners of corporate stock, enjoy the benefit of deferral: their annual unrealized gains are not counted annually as taxable income. But the similarity in the tax treatment of directly held corporate stock and retirement accounts ends later in life.

Starting at age 73, retirement account holders must take mandatory distributions — about $4,000 annually for every $100,000 in account balance (increasing with the age of the holder) — in part so they can’t use their accounts as tax shelters. This begins the process of drawing down the accounts and effectively requires account holders to begin realizing their gains, even if they would not otherwise want to. The distributions flowing out of the accounts, including the original contributions plus the accrued gains, are taxed at ordinary income tax rates.

Moreover, if a retirement account holder dies with an account balance and leaves it to a family member or other heir other than a spouse, the heir must liquidate the account over a ten-year period. The heir also must pay individual income taxes at ordinary income tax rates on the distributions in each of those ten years.

The bottom line for middle-class people who hold stocks in retirement accounts is that, while they enjoy generous tax advantages during their working lives as they build up their accounts, all accrued unrealized capital gains must be realized by either the account holder starting at age 73 or by their heirs within ten years of receiving them. Also, their capital gains income is taxed at ordinary income tax rates, rather than the lower capital gains rate enjoyed by holders of corporate stock held outside of retirement accounts. Turning 73 thus has important tax consequences for middle-class retirement account holders.

In contrast, for wealthy people whose assets consist primarily of direct ownership of stock or other capital assets, 73 is just another birthday. They face no realization requirement for capital gains accrued over a lifetime of owning corporate stock. By the end of their lives, they could have millions, hundreds of millions, or even billions of dollars in unrealized capital gains from their privately held stocks or other assets — income that has never faced the income tax. And after they die, the entire income tax liability on those gains is simply erased, for them and their heirs.

Minimum Tax Would Be Paid Over Time, Raise Significant Revenue

Some critics have claimed that the Biden-Harris proposal to tax unrealized capital gains of extremely wealthy households would be unworkable or require business owners to prematurely sell their investments, such as shares in a closely held company, to pay the tax. The proposal, however, includes several design mechanisms to make it easier to administer.

For instance, the tax would be paid over several years — essentially a down payment on the tax that will be owed when the gains are realized (typically, when assets are sold). Spreading out the payments in this way would also mitigate concerns about wealthy taxpayers who have large gains in one year and losses the next: if a taxpayer later has a large unrealized loss, those losses will also be spread out over several years and future tax payments will be reduced to reflect the losses, with refunds paid to taxpayers who have no minimum tax payments to offset. It would also mitigate concerns that public company founders would have to sell large amounts of stock to pay the tax, because their initial payments would be made over nine years.

Another design feature would allow taxpayers who primarily own non-publicly traded assets — like shares of a closely held company — to defer tax (with a charge akin to interest) until they sell assets. Moreover, the proposal applies only to the approximately 10,000 U.S. taxpayers with $100 million in assets, and these very wealthy people tend to own large amounts of highly liquid assets like publicly traded stock or other financial assets, not shares in small businesses.

The proposal would raise $500 billion over ten years, according to the Treasury Department, generated from a small subset of the wealthiest households in the country — those with more than $100 million in assets — who today often enjoy extremely low average tax rates. Thus, the proposal would not only mark a step toward creating a fairer tax code but would also raise revenue that is badly needed to meet the nation’s commitments to seniors, make high-value investments that will improve well-being and broaden prosperity, and improve the fiscal outlook.

End Notes

Vice President Harris’ campaign has endorsed this proposal in the Administration’s budget. See Twitter post of Joseph Zeballos-Roig, reporter for Semafor, September 4, 2024, https://x.com/josephzeballos/status/1831433950780133752.

Income, according to the textbook definition, is the sum of one’s consumption and change in net worth. This is known as Haig-Simons or economic income and includes both realized and unrealized capital gains, because “whether you sell the asset does not matter because an increase in the value of assets you own increases your purchasing power.” Joel Slemrod and Jon Bakija, Taxing Ourselves: A Citizen’s Guide to the Debate Over Taxes, MIT Press, 2017.

Department of the Treasury, “General Explanations of the Administration’s Fiscal Year 2025 Revenue Proposals,” March 11, 2024, https://home.treasury.gov/system/files/131/General-Explanations-FY2025.pdf.

Capital gains are also taxed at lower rates than ordinary income, topping out at 23.8 percent for the highest earners (including a 3.8 percent net investment income tax on high earners).

Tax Policy Center, “T23-0002 – Distribution of Long-Term Capital Gains and Qualified Dividends by Expanded Cash Income Percentile, 2022,” https://www.taxpolicycenter.org/model-estimates/distribution-individual-income-tax-long-term-capital-gains-and-qualified-78.

Jenny Bourne et al., “More Than They Realize: The Income of the Wealthy,” National Tax Journal, June 2018, https://www.irs.gov/pub/irs-soi/estatestaxbourne.pdf.

Nitasha Tiku and Jay Greene, “The billionaire boom,” Washington Post, March 12, 2021, https://www.washingtonpost.com/technology/2021/03/12/musk-bezos-zuckerberg-gates-pandemic-profits/.

Leonard E. Burman, “Biden Would Close Giant Capital Gains Loopholes—At Least for the Rich,” Tax Policy Center, April 28, 2021, https://www.taxpolicycenter.org/taxvox/biden-would-close-giant-capital-gains-loopholes-least-rich.

While serving as the Senate Finance Committee’s ranking Democrat in 2019, Senator Wyden released a white paper calling for enacting a mark-to-market system for capital gains and raising the capital gains tax rate to the same rates as taxes on ordinary income. Senate Finance Committee Democrats, “Treat Wealth Like Wages,” https://www.finance.senate.gov/imo/media/doc/Treat%20Wealth%20Like%20Wages%20RM%20Wyden.pdf. Under Wyden’s proposal, large capital gains on corporate stock and other securities that wealthy households own would be taxed annually, while non-publicly traded assets would be subject to a deferral charge at the time of sale.

The phase-in reduces a household’s minimum tax liability to the extent that the liability is greater than two times the minimum tax rate times the amount of the household’s wealth that exceeds $100 million.

Separately, the budget also proposes to end, for high-income households, the special discounted tax rate that applies to capital gains. Candidate Harris has endorsed raising the capital gains tax rate for households with more than $1 million in income to 28 percent and the net investment income tax rate for households with more than $400,000 in income to 5 percent, for a combined 33 percent top tax rate on capital gains. Brian Faler, “Harris goes her own way on capital gains tax hike,” Politico, September 4, 2024, https://subscriber.politicopro.com/article/2024/09/harris-considering-more-moderate-capital-gains-tax-increase-00177357.

Alec Schemmel, “‘Beyond Insane’: Economists slam Biden-Harris proposal to tax unrealized investment returns,” Fox News, August 26, 2024, https://www.foxnews.com/politics/beyond-insane-economists-slam-biden-harris-proposal-tax-unrealized-investment-returns.

Martin Sullivan, “Do the Superrich Pay Tax at the Highest Rates?” Tax Notes, May 17, 2021.

Edward J. McCaffery, “The Death of the Income Tax (or, the Rise of America’s Universal Wage Tax),” Indiana Law Journal, revised April 10, 2019, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3242314.

Oracle Corp., Schedule 14A, September 22, 2023, https://www.sec.gov/ix?doc=/Archives/edgar/data/0001341439/000119312523240594/d744477ddef14a.htm. As of September 10, 2024, Oracle stock is trading at a value of $155.89. Bloomberg, “Markets Data, Oracle Corp,” August 29, 2024, https://www.bloomberg.com/quote/ORCL:US.

Edward G. Fox and Zachary Liscow, “No More Tax-Free Lunch for Billionaires: Closing the Borrowing Loophole,” Tax Notes, January 22, 2024, https://www.taxnotes.com/special-reports/individual-income-taxation/no-more-tax-free-lunch-billionaires-closing-borrowing-loophole/2024/01/19/7j3bg. In 1992, Ellison bought 98 percent of the island of Lanai for $300 million.

State and local taxes, like property taxes, are not subject to the constitutional restrictions on federal taxes like the federal income tax. Furthermore, property taxes are generally imposed on the entire assessed value of real property, not only the gain that has accrued since a home’s purchase. The Biden-Harris proposal only applies to gains, or income. It is also important to note that the tax preferences for retirement savings are substantial and mainly benefit people with higher incomes and financially secure retirements.

John Bailey Jones and Urvi Neelakantan, “Portfolios Across the U.S. Wealth Distribution,” Federal Reserve Bank of Richmond, Economic Brief No. 23-39, November 2023, https://www.richmondfed.org/publications/research/economic_brief/2023/eb_23-39

Annual tax rates vary but tend to fall roughly between 0.25 percent and 2.0 percent. Jim Probasco and Mia Taylor, “Property tax rates by state: What to expect in your area,” Bankrate, May 29, 2024, https://www.bankrate.com/real-estate/property-tax-by-state/#tax-by-state.

State of Illinois, “How can the value of property increase when I haven’t made any changes to my property?” https://tax.illinois.gov/questionsandanswers/answer.353.html.

Maryland Department of Assessments and Taxation, “Maryland Property Values Rise 23.4% According to Maryland Department of Assessments and Taxation’s 2024 Reassessment,” December 29, 2023, https://dat.maryland.gov/newsroom/Pages/2023-12-29-Annual-Assessments.aspx.

Tax Policy Center, “Briefing Book: How Do State and Local Property Taxes Work?” https://www.taxpolicycenter.org/briefing-book/how-do-state-and-local-property-taxes-work.

Board of Governors of the Federal Reserve System, “DFA: Distributional Financial Accounts,” June 14, 2021, https://www.federalreserve.gov/releases/z1/dataviz/dfa/compare/chart/#quarter:132;series:Assets;demographic:income;population:all;units:levels.

This discussion does not apply to Roth 401(k)s, under which employees contribute after-tax amounts and capital gains, dividends, and interest accrue tax-free; qualified withdrawals in retirement are also tax-free.

In 2022, the EARN Act raised the starting age for these required minimum distributions from 72 to 73 for account holders who turn 73 before 2033, and to 75 for account holders who turn 73 thereafter. This change benefits a small group of affluent people whose retirements are financially secure without tapping their retirement accounts. See Chuck Marr and Samantha Jacoby, “House Bill Would Further Skew Benefits of Tax-Favored Retirement Accounts,” CBPP, April 29, 2022, https://www.cbpp.org/research/federal-tax/house-bill-would-further-skew-benefits-of-tax-favored-retirement-accounts.

The ability to defer tax on retirement contributions and earnings until earnings are withdrawn is a substantial subsidy because there is no tax on the growth in the account assets over time as they produce earnings and because average tax rates tend to be lower in retirement, when the tax is eventually paid. Tax subsidies for retirement savings are one of the largest federal tax expenditures, costing around $380 billion annually. Michael Doran, “The Great American Retirement Fraud,” October 28, 2022, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3997927.

There are additional limited exceptions to the ten-year liquidation rule for minor children of the original account holder, people with disabilities or chronic illnesses, or people who are less than ten years younger than the original account holder.

The asset may be subject to the estate tax, which theoretically provides a last opportunity to collect some tax on income that has escaped the income tax. However, a decades-long political effort has eviscerated the estate tax so much that Gary Cohn, then-director of President Trump’s National Economic Council, reportedly told Senate Democrats in 2017, “Only morons pay the estate tax.” Julie Hirschfeld Davis and Kate Kelly, “Two Bankers Are Selling Trump’s Tax Plan. Is Congress Buying?” New York Times, August 28, 2017, https://www.nytimes.com/2017/08/28/us/politics/trump-tax-plan-cohn-mnuchin.html.

Once the minimum tax is imposed, households subject to it could make prepayments over nine years for previously accrued gains and five years for gains accrued after enactment.

Jason Furman, “Biden’s Better Plan to Tax the Rich,” Wall Street Journal, March 28. 2022, https://www.wsj.com/articles/bidens-better-plan-to-tax-the-rich-unrealized-capital-gains-assets-treasury-distortion-11648497984?mod=hp_opin_pos_5.

Robert Frank, “The number of people with at least $100 million has doubled since 2003,” CNBC, October 10, 2023, https://www.cnbc.com/2023/10/10/number-of-people-with-100-million-has-doubled-since-2003.html.

Department of the Treasury, op. cit.

Richard Kogan et al., “More Revenue Is Required to Meet the Nation’s Commitments, Needs, and Challenges,” CBPP, June 17, 2024, https://www.cbpp.org/research/federal-budget/more-revenue-is-required-to-meet-the-nations-commitments-needs-and.

Spread the word