Some opponents of the Affordable Care Act’s (ACA) Medicaid expansion who seek to dissuade states that haven’t adopted it from doing so are using inaccurate claims and misleading arguments to make their case. In particular, in a recent paper and Wall Street Journal op-ed, former Trump White House health official Brian Blase claimed that large numbers of “middle-class” people are illegitimately enrolled in Medicaid through the ACA’s Medicaid expansion. Yet the data do not show that large numbers of ineligible people are enrolling.

Blase drew mainly on one study that finds that significant numbers of people who reported in Census surveys that they have annual income above the Medicaid expansion eligibility cutoff (138 percent of the poverty line) appear to have gained coverage through the expansion. The op-ed, which Blase co-authored with Aaron Yelowitz (an author of the study in question), concluded that the expansion has become “an entitlement program for the middle class” and that, as a result, the expansion isn’t achieving its goals.

Those reporting survey income above 138 percent of poverty, however, could be eligible for the Medicaid expansion for many legitimate reasons. They could, for example, be eligible for part of the year because they had low income in some months due to temporary unemployment or unstable hours — Medicaid eligibility is generally based on monthly, not annual, income. Or, they could have income from child support or other sources that don’t count toward Medicaid eligibility. Or, in their responses to the Census questions, they could have provided rough estimates of their incomes rather than precise answers. The Census surveys don’t verify income, while Medicaid does.

In addition, some higher-income people whom surveys record as enrolled in Medicaid may be enrolled in other coverage (such as marketplace coverage), either because they responded incorrectly to the survey questions or because of the way that Census studies infer Medicaid enrollment for those who don’t answer the relevant survey question. A separate study by Yelowitz corrects for some, though not all, of these factors — and that alone cuts in half the number of enrollees who appear to have income above the Medicaid limits.

In their op-ed, Blase and Yelowitz implied that Medicaid enrollment is based on self-reported income but, in fact, state Medicaid programs verify an applicant’s income when he or she applies and then periodically during the year. To make their case about “massive” numbers of people improperly or fraudulently enrolling, the authors also misrepresented the findings of audits by the federal government and the state of Louisiana, as explained below.

In reality, the Medicaid expansion is serving the people that it’s supposed to serve — low-income people who are eligible and need it. States that have adopted the expansion have seen far larger coverage gains, particularly for low-income people, than non-expansion states since the expansion took effect. And across the states, uninsured rates have fallen by about the same amount that Medicaid’s enrollment has risen, indicating that the vast majority of those gaining coverage would otherwise be uninsured. Moreover, research shows that the Medicaid expansion is improving access to medications, check-ups, screenings, and other needed care, reducing medical debt and evictions, and reducing premature deaths among low-income people. If there is a scandal here, it is that millions of low-income people in non-expansion states remain uninsured.

Claims Rest on Problematic Presentation of Data on the Medicaid Expansion

Blase’s claims, detailed in a Galen Institute paper and in the Wall Street Journal op-ed coauthored with Yelowitz, are largely based on a study by Yelowitz and other researchers that uses the Census Bureau’s American Community Survey (ACS) data to examine Medicaid enrollment by income across states. It finds that Medicaid enrollment rose at a greater rate among people with incomes above 138 percent of the poverty line in nine states that expanded Medicaid than in 12 states that didn’t expand. The op-ed erroneously concludes that the study shows that “massive” numbers of “middle-class” people are improperly enrolled in Medicaid. It also references — and misrepresents — studies of Medicaid expansion enrollment by the Department of Health and Human Services (HHS) Inspector General and the Louisiana Inspector General’s office.

Many People Who Report Somewhat Higher Income in Surveys Are Eligible for Medicaid Expansion

Blase and Yelowitz’s claims don’t take into account that the income that people report on a Census survey doesn’t always align with how Medicaid treats income in determining eligibility. There are a number of reasons why people who report incomes somewhat above 138 percent of the poverty line in a survey may be eligible for the Medicaid expansion.

Probably most important, surveys measure annual income, while Medicaid eligibility is primarily based on monthly income. Someone whose annual income is above 138 percent of the poverty line, but who experiences a period of unemployment or underemployment during the year, may well be eligible for Medicaid for part of the year.

Income changes over the course of a year are especially prevalent among low-income people. Low-wage jobs are often unstable, with frequent job losses and work hours that can fluctuate from month to month. Many Medicaid enrollees also work seasonal jobs in industries such as retail or tourism. A study looking at participation of working-age adults in the Supplemental Nutrition Assistance Program (SNAP), which has federal income limits close to those of the Medicaid expansion, found that workers earning low wages are frequently in and out of work and on and off SNAP as their earnings fall and rise. A similar study looking at Medicaid showed similar income volatility.

The majority of people with income below 138 percent of the poverty line at the beginning of a 12-month period had income above 138 percent of the poverty line at some point during those 12 months, another study found. Conversely, about 40 percent of people with incomes between 138 and 200 percent of the poverty line saw their incomes fall below 138 percent of the poverty line at some point over the course of a year. This degree of income volatility means that large numbers of people with annual income above 138 percent of the poverty line might be appropriately enrolled in Medicaid at some point during the year.

There are additional reasons people with survey income above 138 percent of the poverty line could be eligible for Medicaid, including:

- Mismeasurement of income in surveys. People don’t necessarily answer surveys precisely, while they must be precise in a Medicaid application, which is signed under penalty of perjury. In their study, Yelowitz and his coauthors acknowledge that their findings could be attributable in part to survey measurement error in either insurance coverage or income.

- Differences in who counts as part of a household. The ACS asks about the income of all related people who live together; Medicaid uses different household rules that generally only take the income of immediate family members into account. In general, parents’ income counts in determining eligibility for children under 19 (or 21 at state election) and income of each spouse counts in determining the other’s eligibility whenever the family members live together. But, for example, a grandparent under 65 with earnings below 138 percent of the poverty line could be eligible for Medicaid in an expansion state when she lives with her adult children, even when the extended family’s total income exceeds the eligibility limit. The same would be true for a 30-year-old low-wage worker living with his or her parents.

- Medicaid rules that exclude certain types of income in determining eligibility. The ACA changed how Medicaid counts income to align with how the federal income tax system treats income in determining eligibility for premium tax credits, which help pay for health coverage in the ACA marketplaces. The tax rules exclude child support, Supplemental Security Income (SSI) benefits, and certain other forms of income, which can make eligible Medicaid enrollees appear ineligible based on their Census survey responses. Child support, a child’s SSI payment or Social Security survivor’s benefit, some veterans’ payments, and worker’s compensation payments generally wouldn’t be counted in determining Medicaid eligibility but would likely be reported in Census surveys.

The study does not adjust for the impact of these differences between how Medicaid calculates eligibility and how people may report their income on the ACS. Some of these adjustments aren’t possible in the ACS data (which don’t capture monthly income, for example). A prior study conducted by Yelowitz, however, did adjust for some of the differences. These limited adjustments cut in half the number of people who appeared ineligible.

Census Data May Also Exaggerate Number of Higher-Income People Enrolled in Medicaid

In addition, some higher-income people whom Census data record as enrolled in the Medicaid expansion may actually be enrolled in other forms of coverage, due to mistakes about insurance coverage in answers to the surveys and due to ways in which Census infers Medicaid enrollment for people who don’t answer the relevant survey question.

On the ACS, insurance coverage options include “insurance purchased directly from an insurance company” and “Medicaid, Medical Assistance, or any kind of government-assistance plan for those with low incomes or a disability.” This question wording may lead some people purchasing subsidized coverage through the ACA marketplaces to mistakenly place themselves in the Medicaid category, rather than responding that they have private insurance. For these and other reasons, a meaningful share of respondents appear to misreport their source of insurance coverage, as significant differences between survey-based estimates and administrative data show.

For some people who don’t respond to the ACS question about Medicaid receipt, the Census Bureau imputes a response based on various characteristics that do not include income. This approach somewhat exaggerates the number of Medicaid enrollees with higher incomes, including the number of Medicaid expansion enrollees, a Congressional Budget Office analysis concluded.

Medicaid Programs Have Stringent Verification Procedures

Blase and Yelowitz imply in their Wall Street Journal op-ed that Medicaid enrollment is based purely on self-reported income. In particular, they incorrectly assert that people using the HealthCare.gov website who “enter no income simply to explore their options” can enroll in Medicaid with no further eligibility checks. But that’s not how Medicaid works.

To determine eligibility, state Medicaid programs verify an applicant’s reported income against electronic data sources at the time of application and then periodically during the year. When verifying income, state Medicaid agencies compare the sworn attestations that clients make on their application and renewal forms to available electronic data. No further documentation is needed if the income reported by the applicant and the electronic data sources both show income below, at, or above the relevant Medicaid eligibility threshold. If there is a difference — for example, if the applicant claims income below the eligibility level and the data source shows income above it — states request documentation to resolve the difference. Similarly states must ask enrollees for documentation if the state receives information from electronic data sources suggesting the enrollee may no longer be eligible for coverage.

This verification process occurs regardless of whether the application process starts at the federal marketplace or the state Medicaid agency. When someone applies at the federal marketplace and appears eligible for Medicaid, depending on the state, the marketplace either determines eligibility itself or transfers the case to the state Medicaid agency for a final determination. In no case does the federal marketplace simply accept the applicant’s assertions. In the nine states that choose to have the federal marketplace determine eligibility for Medicaid, it applies the state’s own eligibility rules and standard Medicaid verification procedures. Regardless of whether the state or the marketplace determines eligibility, the applicant’s self-reported income is verified.

People With Modestly Higher Incomes Who Remain Enrolled in Medicaid Likely Do So Due to Income Volatility, Not Fraud

Some people reporting higher income in the ACS likely experienced a change in income after their eligibility was determined and then remained enrolled in Medicaid for some period after the change.

As noted, low-income people are particularly likely to experience income changes. As a result, Medicaid eligibility rules can require them to shift back and forth between Medicaid and marketplace coverage multiple times during a year (often referred to as “churn”), requiring them to navigate complex processes to maintain coverage.

Insurance transitions often disrupt the continuity of care and coverage. A study of 2015 churn rates in three states found that about 25 percent of low-income adults changed coverage over the course of a year. Over half of those experiencing a change had a gap in coverage. Coverage changes were associated with changes in physicians, increased use of the emergency room, and decreased medication adherence even for many who didn’t have gaps in coverage. Churn also creates problems for health care providers and Medicaid managed care organizations, limiting their ability to provide effective care and increasing their administrative costs as people cycle in and out of coverage. People who churn in and out of coverage have higher health care costs, some studies suggest.

Some states have decided this churn is so counterproductive that they have changed their eligibility rules to limit the frequency with which households need to change coverage. States have the option to provide children enrolled in Medicaid and the Children’s Health Insurance Program (CHIP) with “continuous eligibility” — a full year of coverage regardless of changes in their family’s income. States can also elect to provide continuous eligibility to adults through a Medicaid waiver. To date, 24 states have adopted continuous eligibility for children in Medicaid, and 26 have adopted it for CHIP. So far, Montana and New York are the only states with continuous eligibility for adults. Utah has a proposal pending.

In states that have not adopted continuous eligibility, it is likely that some people still remain enrolled in Medicaid for a period after their income rises; similarly, it is likely that some people remain enrolled in the marketplaces for a period after their income falls. But while Blase’s paper suggests that the federal government is spending billions on people who are inappropriately enrolled in Medicaid, the reality is that the fiscal impact of these mistakes is limited. Medicaid expansion enrollees whose incomes rise modestly above 138 percent of the poverty line are generally eligible for subsidized marketplace coverage. And for people with low incomes, the federal cost for subsidized marketplace coverage is similar to (or sometimes greater than) the federal cost for Medicaid.

Authors Do Not Accurately Present the Results of Government Audits

The audits conducted by Louisiana and by federal investigatory officials that the Blase and Yelowitz op-ed cites do not support the authors’ claim of “massive improper and fraudulent expansion enrollment.”

While Blase and Yelowitz claim that a 2018 Louisiana audit “found 82 percent of expansion enrollees were ineligible,” it actually raised eligibility questions about one-tenth that number of people. The audit examined only the roughly 10 percent of enrollees who appeared most likely to be ineligible based on the state’s quarterly wage database. It found that 82 percent of that 10 percent had income above the eligibility threshold at some point during the year, not 82 percent of the expansion population.

Moreover, few of these cases were likely the result of deliberate fraud. All of these individuals had their eligibility verified at the time they enrolled, and they likely experienced a subsequent change in income. The audit also does not reflect Louisiana’s current eligibility procedures: Louisiana’s new eligibility system, which went live late in 2018 — after the audit was completed — now regularly reviews the eligibility of enrollees whose incomes may have risen.

Similarly, both the Wall Street Journal op-ed and the Galen Institute paper cite 2018 HHS Inspector General audits of California and New York, which Blase claims found that 25 percent of expansion enrollees were ineligible. In reality, both audits mostly identified cases where the states miscategorized people who were eligible for Medicaid, but under a different eligibility category, as expansion enrollees. That’s still concerning, because the federal government pays a higher share of costs for expansion enrollees than other enrollees (with states paying the remainder). But it is inaccurate to suggest, as Blase does, that these studies show that a quarter of individuals were ineligible for the Medicaid program.

Data Show That Medicaid Expansion Benefits Low-Income People Who Would Otherwise Be Uninsured

The broader thesis of both the Wall Street Journal op-ed and the Galen Institute paper is that the Medicaid expansion is not achieving its goals, and money spent on Medicaid expansion isn’t well-spent. A large body of evidence refutes these claims.

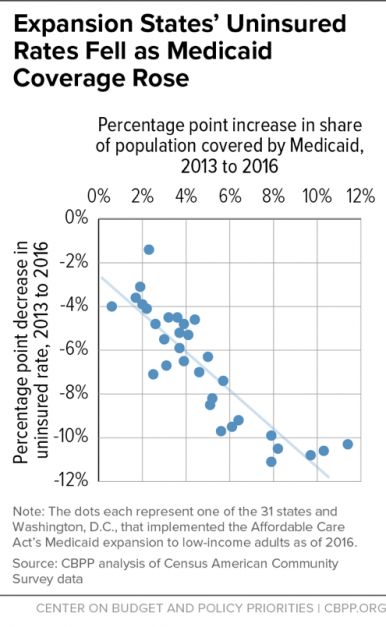

FIGURE 1

Since expansion took effect in 2014, uninsured rates have fallen far more in states that have expanded Medicaid than in non-expansion states, particularly for low-income people. Since 2013, Medicaid coverage among adults with incomes under 138 percent of poverty in Medicaid expansion states has increased about 18 percentage points, while uninsurance has dropped about 19 percentage points. In non-expansion states, by contrast, low-income adults haven’t fared as well — with uninsurance falling by only about 11 percentage points, or only a little more than half as much as in expansion states. Uninsured rates have fallen in all states due to provisions of the ACA that apply nationwide, such as its subsidized coverage through the health insurance marketplaces.

In the op-ed, Blase and Yelowitz also imply that large numbers of people have signed up for Medicaid expansion despite having other coverage options, arguing that Medicaid expansion has worked against the preservation of private coverage. But, as Figure 1 shows, there is a strong linear and nearly one-to-one relationship between the increase in the share of a state’s population that’s covered by Medicaid and the decrease in the share that’s uninsured. This analysis, which incorporates people at all income levels, suggests that the large majority of those gaining coverage under Medicaid expansion would otherwise have been uninsured.

That is the same conclusion reached by several studies that have directly investigated whether Medicaid expansion has “crowded out” private coverage. Most of these studies find “no evidence of ‘crowd-out,’” while others show “slight declines in private coverage” from Medicaid expansion, a comprehensive Kaiser Family Foundation literature review concludes.

Meanwhile, a growing body of research finds that expansion is yielding substantial gains for beneficiaries. Expanding coverage has improved financial security, reducing medical debt and evictions. It has increased the share of low-income adults who have a personal physician, get check-ups, and receive recommended preventive care such as cholesterol and cancer screenings, and it has decreased the share delaying needed care or skipping medications due to cost. Evidence is building that these gains in access to care are translating into improved health outcomes, including significant reductions in premature deaths among older adults.

Had the uninsured rate in non-expansion states fallen since 2013 to the same degree that it fell in Medicaid expansion states, 4.7 million fewer Americans would have been uninsured last year. Misleading claims about who is enrolled in the Medicaid expansion should not deter additional states from extending these benefits to the millions of people who continue to be left out.

Judith Solomon is a Senior Fellow at the Center on Budget and Policy Priorities, where she focuses on Medicaid and other health programs with a focus on policies to make coverage and health care services available and affordable for low-income people.

She has testified before state legislatures and spoken extensively to national and state nonprofit groups and is often cited by national and state media, including the New York Times, USA Today, Wall Street Journal, and Washington Post.

Previously, Solomon was a Senior Policy Fellow at Connecticut Voices for Children and Executive Director of the Children’s Health Council. She directed the Council’s work on policy analysis, outreach, education and training, and independent oversight of health care services provided through Connecticut’s Medicaid managed care program.

She has also worked as a legal services attorney specializing in the area of public benefits and taught at the Yale University School of Medicine.

Solomon is a graduate of the University of Connecticut and Rutgers University School of Law in Newark.

You can follow her on Twitter @JudyCBPP.

Matt Broaddus joined the Center in December 1999 and is a Senior Research Analyst in the Health Division.

His policy, research, and analytical work is conducted in the areas of Medicaid and the State Child Health Insurance Programs.

He graduated from Stanford University with an MA in Sociology and a BA in Comparative Literature.

The Center on Budget and Policy Priorities (CBPP) a nonpartisan research and policy institute. We pursue federal and state policies designed both to reduce poverty and inequality and to restore fiscal responsibility in equitable and effective ways. We apply our deep expertise in budget and tax issues and in programs and policies that help low-income people, in order to help inform debates and achieve better policy outcomes. Support CBPP by clicking here.

Spread the word