House Ways and Means COVID Relief Bill Includes Critical Expansions of Child Tax Credit and EITC

Two key tax credit provisions in the COVID relief legislation that the House Ways and Means Committee will consider this week would provide significant help to those on the fault lines of some of the pandemic’s worst economic effects. People who have lower incomes, are Black or Latino, have less than a college education, or work in face-to-face service occupations have long faced barriers to high-paying jobs and opportunity, which the pandemic and its economic fallout have widened. The House bill’s provisions making the full Child Tax Credit available to all children except those with the highest incomes (sometimes called making the credit “fully refundable”), and making an expanded Earned Income Tax Credit (EITC) available to far more low-paid childless workers, would result in historic reductions of child poverty and provide timely income support for millions of people, including millions of essential workers.

The current Child Tax Credit and EITC together lift more children above the poverty line, 5.1 million, than any other economic support program. This level of poverty reduction was achieved through multiple expansions of the EITC and Child Tax Credit since their respective enactments in 1975 and 1997. The House’s proposal — with one significant change to the Child Tax Credit — would lift another 4.1 million children above the poverty line, cutting the remaining number of children in poverty by more than 40 percent. Permanently enacting this historic proposal — along with the EITC provision which would stop the federal tax code from taxing millions of childless adults into or deeper into poverty — would be a landmark achievement and should be an urgent priority once this temporary legislation is enacted.

These expansions will help many hard hit by the current crisis. Many in essential jobs have faced a higher risk of infection and death due to their jobs, while many others lost their jobs or saw their incomes fall due to pandemic-related closures or reduced hours. Jobs in low-paying industries were down more than twice as much between February 2020 and January 2021 as jobs in medium-wage industries and nearly four times as much as in high-wage industries. Due to employment discrimination and unequal opportunity in education and housing, among other factors, gaps in unemployment between Black and Hispanic workers on one hand and white workers on the other widen quickly in recessions and narrow much more slowly after an economic recovery begins. Today the Black unemployment rate remains at 9.2 percent and the Hispanic rate at 8.6 percent, while the white unemployment rate has fallen back to 5.7 percent.

The two tax credit expansions, in legislation that the House Ways and Means Committee will. mark up this week and combine with other committee bills to form the full relief bill, would do much to alleviate these harmful effects. They would:

Make the full Child Tax Credit available to all children except those with the highest incomes. Some 27 million children — including roughly half of all Black and Latino children and a similar share of rural children — receive less than the current maximum $2,000-per-child tax credit because their parents earn too little, even as middle- and higher-income families get the full amount. The proposal would make the full Child Tax Credit available to children in families with low earnings or that lack earnings in a year, and it would increase the credit’s maximum amount to $3,000 per child and $3,600 for children under age 6. It would also extend the credit to 17-year-olds. The increase in the maximum amount would begin to phase out for heads of households making $112,500 and married couples making $150,000. The proposal would lift 4.1 million children above the poverty line — cutting the number of children in poverty by more than 40 percent. The proposal also would lift 1.1 million children above half the poverty line (referred to as “deep poverty”). Black and Latino children in particular, whom the current credit disproportionately leaves out or leaves behind, would benefit.

Make an overdue EITC increase for low-paid working adults not raising children in the home. The EITC is a powerful wage subsidy with a glaring flaw: it largely excludes so-called “childless adults,” providing only a tiny credit to a very small number of these workers. The House’s relief bill would fix this flaw at a critical time by raising the maximum EITC for childless adults from roughly $530 to roughly $1,500, and the income cap for these adults to qualify from about $16,000 to at least $21,000. It also would expand the age range of eligible childless workers to include younger adults aged 19-24 who aren’t full-time students, as well as people aged 65 and over. This would provide timely income support to over 17 million people who do important work for low pay, including the 5.8 million people who are currently the lone group that the federal tax code taxes into, or deeper into, poverty, in large part because their EITC is too low.

Expanded Child Tax Credit Would Cause Historic Reduction in Child Poverty

Low-income children, disproportionately children of color, have been particularly hard hit by the pandemic and its related economic and educational harms. Between 9 and 12 million children live in a household where the children didn’t eat enough because the household couldn’t afford it, according to the most recent Census data. Many of these same children also have a higher risk of losing school instruction time due to the pandemic; “earning loss will probably be greatest among low-income, black, and Hispanic students,” one analysis found.

Raising the incomes of children growing up in poverty through policies such as the Child Tax Credit can make an important difference in children’s lives now and in the long term, a congressionally chartered report issued in 2019 by a National Academy of Sciences’ (NAS) panel on child poverty explained. “The weight of the causal evidence does indeed indicate that income poverty itself causes negative child outcomes, especially when poverty occurs in early childhood or persists throughout a large portion of childhood,” concluded the panel. The better outcomes that are linked with stronger income assistance include healthier birthweights, lower maternal stress (measured by reduced stress hormone levels in the bloodstream), better childhood nutrition, higher school enrollment, higher reading and math test scores, higher high school graduation rates, less use of drugs and alcohol, and higher rates of college entry. The NAS panel devised two packages of policy proposals aimed at cutting child poverty in half, one of which included as a centerpiece a $2,700-per-child “child allowance” that is very similar to the expanded Child Tax Credit proposal under consideration. (The NAS plan included several other substantial components, including an EITC expansion, that taken together are larger than the current Child Tax Credit proposal.)

The House plan’s Child Tax Credit expansion would deliver significant additional income to low-income children and their families. It would make the full credit available to 27 million children — including roughly half of all Black and Latino children and a similar share of children who live in rural areas — whose families now don’t get the full credit because their parents lack earnings or have earnings that are too low.

Among the 4.1 million children whom the expansion would lift above the poverty line, 1.2 million are Black and 1.7 million are Latino. Of the 9.9 million children it would lift above or closer to the poverty line, 2.3 million are Black, 4.1 million are Latino, and 441,000 are Asian American.

To see what this can mean to individual families, consider these examples:

- A single mother of a toddler, who earns $10,000 a year providing in-home care to older people (with work hours that fluctuate significantly from month to month), now receives a Child Tax Credit of $1,125. Under the House plan, she’d receive $3,600, a gain of $2,475.

- A single mother with a 4-year-old daughter and 8-year-old son, who is out of work for the year due to a health condition, now receives no Child Tax Credit at all, adding to the family’s financial insecurity. Under the House plan, she would receive the full Child Tax Credit of $3,600 for her daughter and $3,000 for her son to help with the children’s expenses.

A married couple in which one spouse earns $20,000 as a short-order cook and the other cares for their 3-year-old son and 7-year-old daughter now receives a credit of $2,625 — well below the $4,000 credit that a higher-income family with two children receive. Under the House plan, they would receive the full Child Tax Credit of $3,600 for their son and $3,000 for their daughter, or a family gain of $3,975.

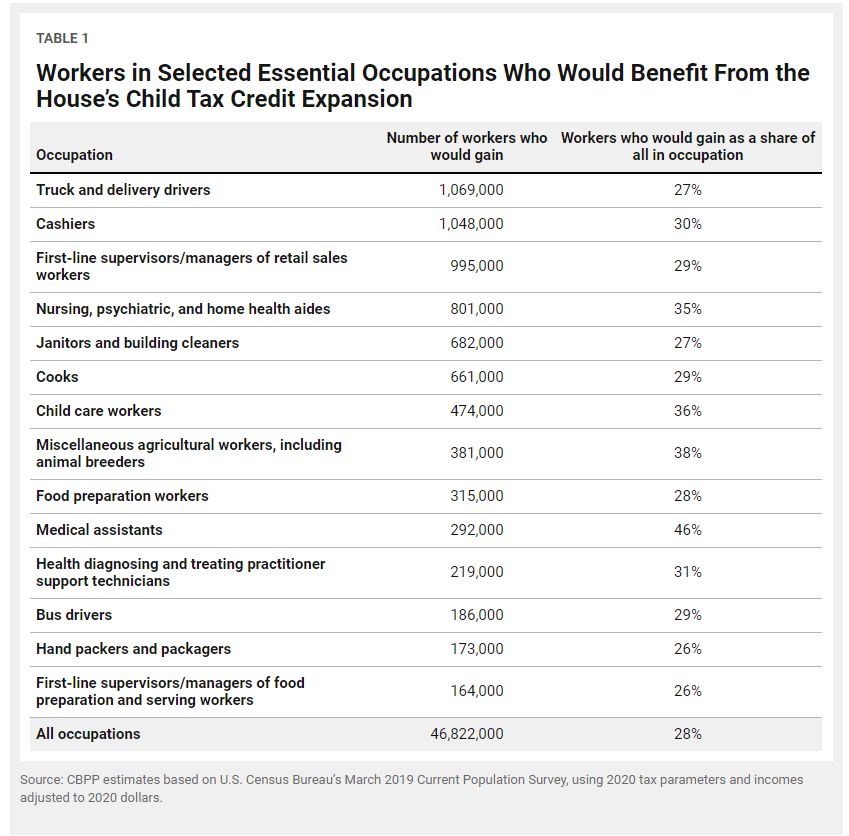

The Child Tax Credit expansion would provide important help to people in a myriad of jobs that pay little and often have fluctuating schedules, including people caring for the elderly, driving buses, cooking and serving meals, and doing many other kinds of important work. (See Table 1.) These occupations are also not conducive to remote work, raising people’s risk of infection during the current crisis.

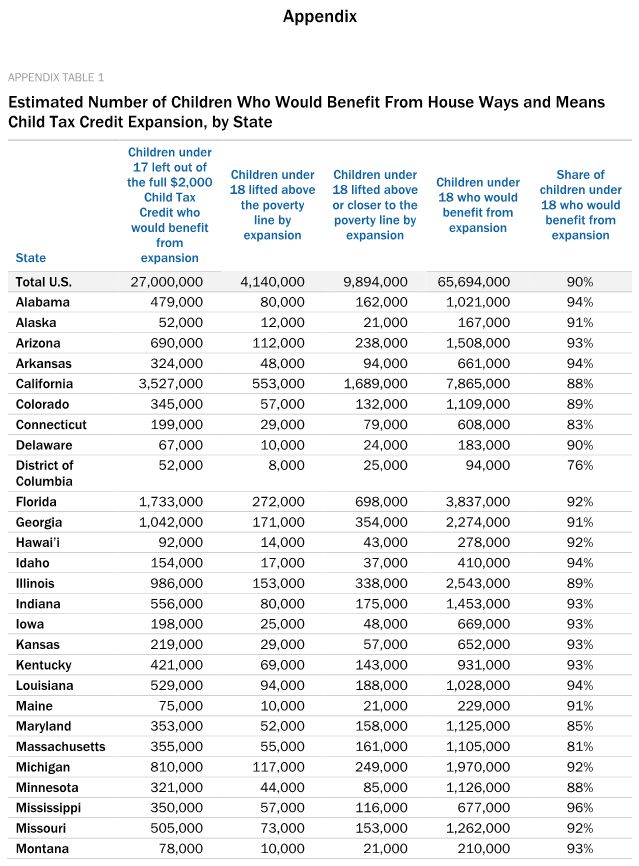

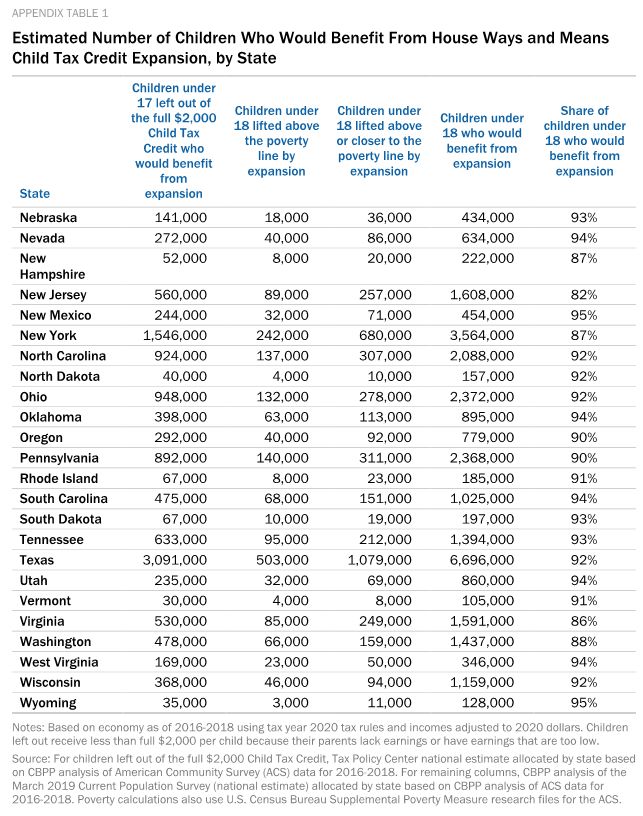

An estimated 65.7 million children would receive a larger Child Tax Credit under the expansion, delivering economic support to large numbers of children in every state. (See Appendix Table 1 for state-by-state estimates.)

================================================================================================

Protect Families With Low Incomes From Repaying Large Amounts They Receive in Advance

The House Ways and Means proposal would provide families with advance payments of their Child Tax Credit for tax year 2021. Between July and December 2021, these advance payments would be provided monthly (or perhaps less frequently, if the IRS has implementation challenges) to the tax filer who claimed the child on a previous year tax return (2020 or, if not available, 2019).

One drawback to providing families with advance payments of their Child Tax Credit is that when tax filers submit their tax return for the year in which they received advance payments, they could end up ineligible for those payments. While changes in income could affect the amount of the credit someone is eligible for, the more significant issue will arise when a child who lived with the tax filer in the prior year does not live with that same tax filer in the year for which the advance payments were made. For example, a child’s father may have claimed the child in the prior year (2020) but the child may live with her mother in 2021. In this case, the father may receive advance payments for the 2021 Child Tax Credit but then learn that he is ineligible for the tax credit when he files his 2021 tax return because the child did not live with him this year. Without appropriate safeguards, low-income tax filers in this situation could owe large amounts to the IRS to repay the federal government for advance payments they received.

More than 3 million children in any given year live with a different adult than they lived with the prior year, we estimate using longitudinal Census data, and a large share have modest incomes.a The Ways and Means Committee has created some important safeguards to protect these low-income tax filers who receive advance payments and are later found ineligible, limiting the extent to which they will have to repay the federal government. Under the legislation, single individuals with incomes below $40,000, heads of households with incomes below $50,000, and married couples with incomes below $60,000 would not have to repay amounts received in advance. And for those with incomes above these thresholds, the amount they have to repay would phase in, though the repayments could be significant for some households. A single individual with income of $55,000 who received $1,500 in advance payments for a child who no longer lives with them would owe back $250, and if the tax filer’s income were $60,000, they would owe back $500. (A tax filer would owe these amounts back to the IRS even if they spent the advance payment toward care for the child.) These safeguards will mean that a large share of those who would be at risk for owing money back will either not be required to repay the advance payments or will only have to repay a partial amount.

The bill also provides a mechanism for families to opt out of the advance payment, but it is likely that many tax filers will not understand the provision or mechanism for opting out well enough to know if they should exercise this option.

For a temporary provision that the federal government must implement quickly, it is arguable that repayment should not be required at all. Both rounds of stimulus payments took this approach — the payments were based on prior-year information and if a tax filer received more than they would have based on their current circumstances, they were not required to repay the amounts. In a temporary provision where advance payments are sent automatically, families are unlikely to understand that such a credit is an advance on their tax return, and they may owe money back upon filing their taxes next year.

If repayment is required, the safeguards that Ways and Means put in place are a good start. They could be strengthened by phasing in repayment more slowly and not requiring repayment if the child lived with the tax filer for part of the year (but less than the six months required to be eligible for the credit).

Most importantly, in a permanently expanded Child Tax Credit that allows advance payments, further steps will be needed to reduce the number of people who receive advance payments and then are found ineligible for the credit and to ensure that those who are in this situation are not asked to repay amounts they cannot afford.

a CBPP calculation based on Census’ Survey of Income and Program Participation data for children who changed parents between 2013 and 2014.

================================================================================================

A Meaningful EITC for Childless Adults

The House plan would expand the EITC for over 17 million adults not raising children at home who work hard at important, but low-paid, jobs. The EITC is a highly successful wage subsidy that’s earned bipartisan support over the years, but the current credit largely excludes adults who aren’t raising children in their homes, and it completely excludes young childless adults trying to gain a toehold in the labor market.

Adults not raising children are the lone group that the federal tax code actually taxes into, or deeper into, poverty, partly because their EITC is so meager. Some 5.8 childless adults aged 19-65 — including 1.5 million Latino and over 1 million Black childless adults — are taxed into or deeper into poverty.

The proposal would raise the maximum EITC for childless adults from roughly $530 to roughly $1,500 and raise the income limit to qualify for the childless workers’ EITC from about $16,000 to at least $21,000. It also would expand the age range of childless workers eligible for the tax credit to include younger adults aged 19-24 who aren’t full-time students, as well as people 65 and over.

To see how this would benefit these workers, consider a 25-year-old single woman who works roughly 30 hours a week throughout the year as a cashier at a convenience store and earns about $9 an hour. Her annual earnings of $13,700 are just above the poverty line of $13,621 for a single individual. But federal taxes push her into poverty:

- Some $1,048 — 7.65 percent of her earnings — is withheld from her paychecks for Social Security and Medicare payroll taxes.

- When filing income taxes, she can claim the $12,400 standard deduction, which leaves her with $1,300 in taxable income. Since she is in the 10 percent tax bracket, she owes $130 in federal income tax.

- Thus, her combined federal income and payroll tax liability, not counting the EITC, is $1,178. She gets a small EITC of $160, so her net federal income and payroll tax liability is $1,018.

- In other words, her earnings were just above the poverty line, but federal taxes push her income about $940 below the poverty line.

- Under the House plan, her EITC would grow to $1,145, raising her income after federal income and payroll taxes to $46 above the poverty line.

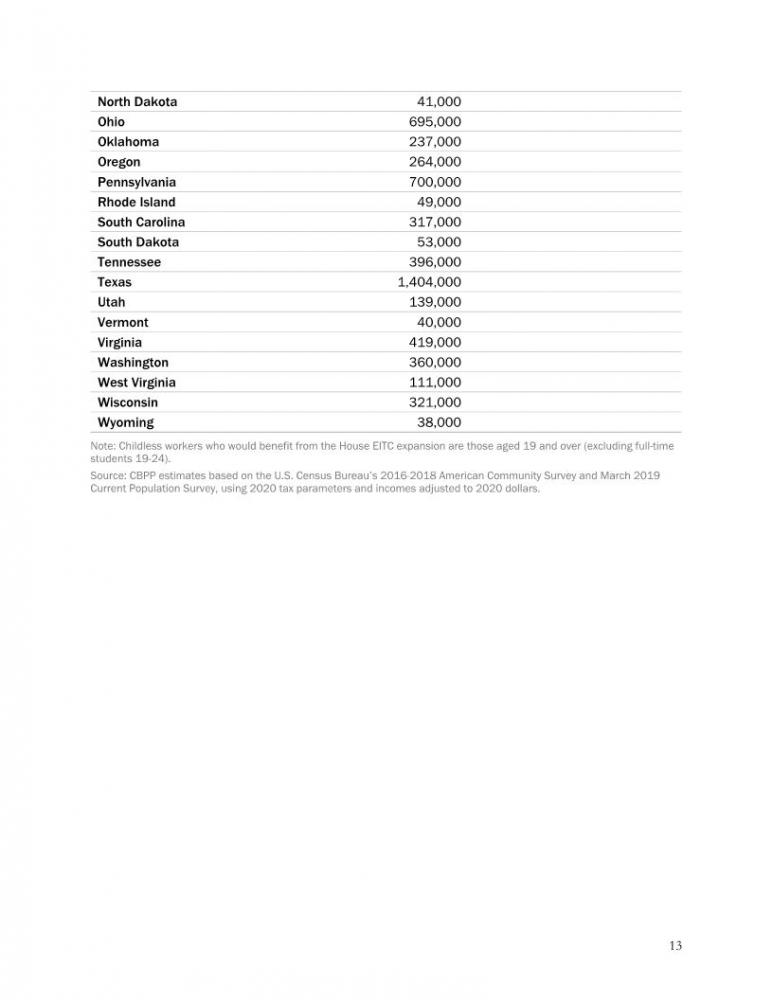

All told, the House Ways and Means proposal would benefit 17.4 million working childless adults across the country, including 4.0 million Latino, 3.0 million Black, and 746,000 Asian American childless adults. (See Appendix Table 2 for state-by-state numbers.)

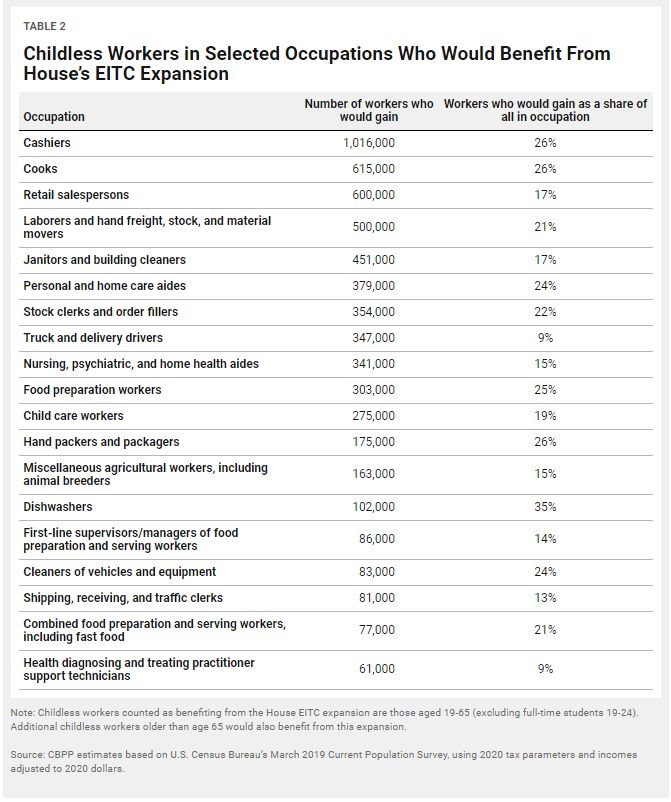

The top occupations that would benefit include cashiers, food preparers and servers, and home health aides. (See Table 2.) The pandemic has helped the nation better understand and appreciate these workers and millions of others who work for low pay and the essential role they play in keeping this economy running, even while they often lack benefits that many other workers take for granted, such as paid sick days. They deserve more than the meager EITC in current law, and the House’s relief proposal would provide concrete, meaningful help.

End Notes

Chad Stone, “Jobs Recovery Still Long Way Off, Especially for Low-Wage Workers and Workers of Color,” Center on Budget and Policy Priorities, February 5, 2021, https://www.cbpp.org/blog/jobs-recovery-still-long-way-off-especially-for-low-wage-workers-and-workers-of-color.

Center on Budget and Policy Priorities, “Tracking the COVID-19 Recession’s Effects on Food, Housing, and Employment Hardships,” updated January 28, 2021, https://www.cbpp.org/research/poverty-and-inequality/tracking-the-covid-19-recessions-effects-on-food-housing-and.

Emma Dorn, “COVID-19 and student learning in the United States: The hurt could last a lifetime,” McKinsey & Co., June 1, 2020, https://www.mckinsey.com/industries/public-and-social-sector/our-insights/covid-19-and-student-learning-in-the-united-states-the-hurt-could-last-a-lifetime#.

National Academies of Sciences, Engineering, and Medicine, A Roadmap to Reducing Child Poverty, National Academies Press, 2019, https://www.nap.edu/read/25246.

Senator Mitt Romney proposed a similar expansion in the Child Tax Credit, making it fully available to all low-income children and increasing the amount from $2,000 to $3,000 for children between ages 6 and 17 and to $4,200 for children under 6. The major differences between the temporary House plan and the permanent Romney plan are that the Romney plan provides the increase to families with much higher incomes, beginning to phase out for married couples making $400,000, and that it pays for the proposal with sharp cuts in other income support programs for low-income families, including a 65 percent cut in the EITC and the elimination of the Temporary Assistance for Needy Families (TANF) block grant. States use TANF to provide income assistance to 1.1 million families with children who have very low incomes and fund a set of other services, including child care, transportation assistance, and services for children at risk of being removed to foster care and their families.

Racial and ethnic categories do not overlap. Figures for each racial group such as Black or Asian American do not include individuals who identify as people of Latino ethnicity. Latino includes all people of Hispanic, Latino, or Spanish origin regardless of race. Figures for children who identify as AIAN alone are not shown because of concerns about sample size and data reliability and because limiting the figures to a single race and ethnicity has particularly strong implications for the estimated size of the AIAN population. Among the roughly 2,050,000 children who identify as AIAN alone or in combination, regardless of Latino ethnicity, 344,000 (17 percent) would be lifted above or closer to the poverty line by the House’s Child Tax Credit expansion. Following the mutually exclusive approach used for other racial and ethnic groups, about 684,000 children identify as AIAN alone, not Latino, and 111,000 (16 percent) of them would be lifted above or closer to the poverty line by the House’s Child Tax Credit expansion.

CBPP estimates based on U.S. Census Bureau’s March 2019 Current Population Survey, using 2020 tax parameters and incomes adjusted to 2020 dollars. These calculations use the Supplemental Poverty Measure, which counts more forms of income than the “official” poverty measure (among other differences).

This estimate excludes full-time students aged 19-23, who under current law can be claimed by their parents as qualifying children for the larger EITC for families with children.

Senator Mitt Romney proposed to significantly reduce the EITC for families with children while expanding the EITC for childless adults. His proposal would raise the maximum EITC for childless adults from roughly $530 to $1,000 for a single filer and $2,000 for a married couple, and raise the income limit to qualify for the childless workers’ EITC for a single filer from about $16,000 to $17,000 and for a married couple from about $22,000 to $34,000. His proposal also increases the phase-in and phase-out rates for the credit.

Racial and ethnic categories do not overlap. Figures for each racial group such as Black or Asian American do not include individuals who identify as people of Latino ethnicity. Latino includes all people of Hispanic, Latino, or Spanish origin regardless of race. Figures for childless workers who identify as AIAN alone are not shown because of concerns about sample size and data reliability and because limiting the figures to a single race and ethnicity has particularly strong implications for the estimated size of the AIAN population. Among the roughly 1.8 million childless workers aged 19 and over (excluding full-time students aged 19-24) who identify as AIAN alone or in combination, regardless of Latino ethnicity, 485,000 (26 percent) would benefit from the House’s EITC expansion for such workers. Following the mutually exclusive approach used for other racial and ethnic groups, about 676,000 childless workers aged 19 and over (excluding full-time students aged 19-24) identify as AIAN alone, not Latino, and 186,000 (27 percent) of them would benefit from the House’s EITC expansion for such workers.

Areas of Expertise

Recent Work:

-

House Ways and Means COVID Relief Bill Includes Critical Expansions of Child Tax Credit and EITC

-

President-Elect’s Plan Includes Vital EITC Increase for Adults Not Raising Children

Areas of Expertise

Recent Work:

-

House Ways and Means COVID Relief Bill Includes Critical Expansions of Child Tax Credit and EITC

-

A Frayed and Fragmented System of Supports for Low-Income Adults Without Minor Children

-

Aggressive State Outreach Can Help Reach the 12 Million Non-Filers Eligible for Stimulus Payments

Recent Work:

-

House Ways and Means COVID Relief Bill Includes Critical Expansions of Child Tax Credit and EITC

-

A Frayed and Fragmented System of Supports for Low-Income Adults Without Minor Children

Recent Work:

-

House Ways and Means COVID Relief Bill Includes Critical Expansions of Child Tax Credit and EITC

-

Needs of Younger Generations Argue for Further Fiscal Relief and Stimulus

Areas of Expertise

Recent Work:

Spread the word